The financial world runs on waiting. You wait for clearance, confirmation, borders to open for your money to cross, etc. This friction is both annoying and expensive. Blockchain cuts through the wait. It enables value to move as seamlessly as information, turning days into minutes and doubt into automated certainty.

The debates in Washington over stablecoin regulation show just how central crypto has become to high-level financial discussions. With so much attention focused on this emerging space, financial enterprises must stay updated on developments as they unfold. The current moment offers more than just a need to follow the news. It presents a concrete opportunity to explore how blockchain can be integrated into existing financial operations. The time to consider its implementation is now.

In this article, we turned to our blockchain consulting experts and discussed the types of blockchain technology, the tangible benefits that blockchain apps offer the financial domain, and successful cases that are already active in fintech. Let’s dive deep into the details.

Blockchain apps are reshaping financial industries

Although it is hard to imagine a situation where cryptocurrency will entirely substitute fiat currencies, the blockchain technology is already used by traditional financial institutions.

- Banks (JP Morgan, Barclays, etc.) apply blockchain for securing sensitive data and automating processes through crypto banking software development.

- The accounting domain uses blockchain as the third party in the Triple Entry Accounting model. This trusted technology serves as the only source of data to secure transactions, confirm, and validate the information of a business’s financial records.

- Investors turn to blockchain for new opportunities (cryptocurrencies, NFTs, utility tokens, etc.).

Here are the most prominent use cases of blockchain technology in financial software development services:

Trade finance & supply chain

Smart contract development allows for replacing paper-heavy processes like Letters of Credit. These automated agreements trigger payments instantly upon verified delivery, tracked in real-time on an immutable ledger. As a result, the processing time shortens from weeks to days, the possible errors decrease, and the terms of the agreements are verified automatically.

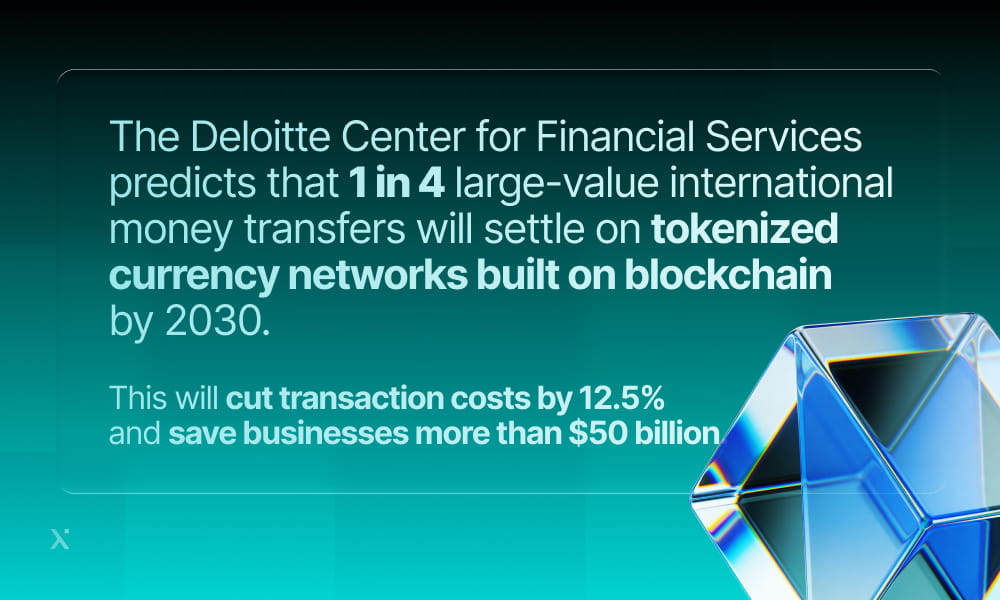

Cross-border payments & remittance

Blockchain integration services enable businesses to bypass the correspondent banking network. Direct peer-to-peer value transfer results in fast transaction settings and cuts fees required for international money transfers. It forms the economics of the global money movement.

Capital markets

Tokenization services break down barriers. Tokenization fragments high-value assets like real estate or bonds into digital tokens, enabling fractional ownership. This democratizes access for investors and injects liquidity into traditionally illiquid markets. Another trading-side application is crypto arbitrage bot development, where automation helps capture price discrepancies across venues.

Regulatory compliance & audit (RegTech)

Blockchain technologies turn compliance from a costly burden into a streamlined function. An immutable audit trail provides a single, tamper-proof record for KYC/AML. Smart contracts can automate reporting, ensuring accuracy and real-time transparency for regulators, which is especially relevant for banking-focused products that need to align controls and reporting with Basel III requirements.

Secure identity management

Another application of blockchain is a secure way for identity verification. Self-sovereign identity allows a white label crypto exchange development company help individuals own and control their verified credentials, sharing them instantly and securely with institutions. This simplifies onboarding and reduces identity fraud.

Fintech’s New Brain: Why Machine Learning is the Real Reason Your Bank Suddenly Understands You

Top 10 Blockchain Development Companies in 2026

Advantages of blockchain in fintech

Blockchain app development services in the financial domain have matured over the years.

- First of all, the benefits of blockchain lie in its advanced cryptography methods. The records are secured against any fraudulent activities.

- Second, the transactions recorded on the blockchain are verified by network participants, which makes them transparent and allows financial institutions to have a reliable source of truth.

- Another benefit is reduced costs. By streamlining processes and automating verification, blockchain reduces reliance on traditional intermediaries. This cuts processing time and overhead, leading to lower costs for end-users.

- Automation that is achieved with smart contracts eliminates the risks associated with manual transactions and increases the general efficiency.

- Finally, blockchain technology creates an immutable audit ledger of all transactions and operations. This makes the process of compliance regulation clear and structured.

Here is a table comparing traditional and fintech blockchain software development.

| Feature | Traditional fintech app | Blockchain-powered fintech app |

| Trust & transparency | Centralized authority, opaque internal processes | Decentralized consensus, transparent & immutable ledger |

| Security | Firewalls, databases (vulnerable to single-point attacks) | Cryptographic hashing, distributed storage (tamper-evident) |

| Automation | Requires API integrations, manual oversight | Programmable smart contracts for automatic execution |

| Settlement speed | Often batch-processed; can take days | Near real-time, 24/7 |

| Operational costs | High intermediary and reconciliation costs | Reduced intermediaries, lower transaction costs at scale |

| Development & complexity | Established frameworks, predictable scaling | Emerging talent pool, new architectural paradigms (gas fees, consensus) |

| Regulatory landscape | Generally clear | Evolving and varies significantly by jurisdiction |

Building the Unbreakable Exchange: A Developer's Guide to Canton Network

Your Practical Guide to Creating a Decentralized Cryptocurrency Exchange

Examples of successful industry applications

Let’s look at the most successful blockchain apps in finance and get to know their secret ingredient.

AZA Finance (formerly BitPesa)

AZA succeeded by targeting a specific, painful bottleneck: cross-border payments and payment software development in and out of Africa. Traditional channels were slow and expensive. By using blockchain as a settlement layer, AZA creates direct corridors between local currencies. The solution bypasses multiple correspondent banks. This results in reduced transfer times and fees and opens economic corridors that others find too complex.

we.trade

This platform allows European SME trade organizations to build trust between each other. The platform uses smart contracts. They automate payments upon the digital confirmation of shipment or delivery, as agreed. Buyers do not hesitate to pre-pay, and sellers do not risk delivering goods without payment. This model perfectly illustrates the value of blockchain eCommerce development, as it allows smaller businesses to trade confidently by removing the traditional risks associated with cross-border transactions.

Kinexys by J.P. Morgan

J.P. Morgan’s success with Kinexys demonstrates blockchain’s power for internal efficiency at scale. Built on its private blockchain, J.P. Morgan uses Kinexys to instantly verify ownership of trillions of dollars in financial assets. This eliminates the traditional, error-prone process of reconciling data across departments and external parties. It frees capital and reduces operational risk. It proves blockchain’s strength as a single source of truth within large institutions.

Axoni

Axoni’s success is infrastructure-focused. It recognized that capital markets run on synchronized data between institutions. Its blockchain-based platforms, like AxCore, replace the brittle messaging used for equity swaps or syndicated loans with a shared record of the transaction. This eliminates reconciliation failures and lifecycle event errors.

HSBC Orion

HSBC applied blockchain to private placements and digital bonds. Orion’s success comes from using tokenization to represent ownership directly on a blockchain. This allows for instantaneous settlement and automated coupon payments via smart contracts. The result is increased efficiency and new possibilities, like fractional ownership, in a market traditionally bogged down by manual and paper-driven processes.

Ant Group

Through its AntChain platform, Ant Group has successfully scaled blockchain for massive, real-world supply chain finance. Its application allows banks to see an immutable record of transactions and logistics events along a supply chain. This shared visibility reduces the risk of financing for SMEs, as lenders can trust the verified data on-chain. It turns opaque supply chains into transparent, financeable assets.

While the examples above focus largely on enterprise and institutional use cases, the same principles of trust and disintermediation apply equally well to P2P crypto exchange development, where the goal is to connect individual buyers and sellers directly through escrow-protected workflows and verifiable dispute resolution.

Below is the summarizing table of the technologies behind these successful apps and the impact they have made.

| Key technology & real-world examples | What it enables | Why it’s a game-changer |

| Smart contracts (we.trade, Santander) | Self-executing contracts that automatically trigger actions (like payments) when pre-set digital conditions are met. | Eliminates manual processing, cuts delays and errors, and builds trust by removing the need for intermediaries to enforce agreements. |

| Immutable ledger (Kinexys, HSBC) | A permanent, unchangeable record of all transactions that is shared and synchronized across a network. | Creates a foundational layer of trust, drastically reduces fraud and reconciliation costs, and simplifies auditing and regulatory compliance. |

| Tokenization (HSBC Orion, Ant Group). | Converts rights to a real-world asset (securities, invoices, etc.) into a unique digital token on the blockchain. | Unlocks liquidity for illiquid assets, enables 24/7 markets, fractional ownership, and allows for programmable features like automated dividends. |

| Decentralized Settlement (AZA Finance, Santander) | Enables the direct peer-to-peer transfer of value without relying on a central clearing authority or correspondent banking network. | Slashes transaction times from days to minutes and significantly reduces costs by removing intermediaries from the payment chain. |

A Network of Networks: How Canton Is Redesigning Financial Infrastructure

Crypto Wallets Get Brain: How AI Crypto Wallet Development is Creating a Smarter and Safer Financial Future

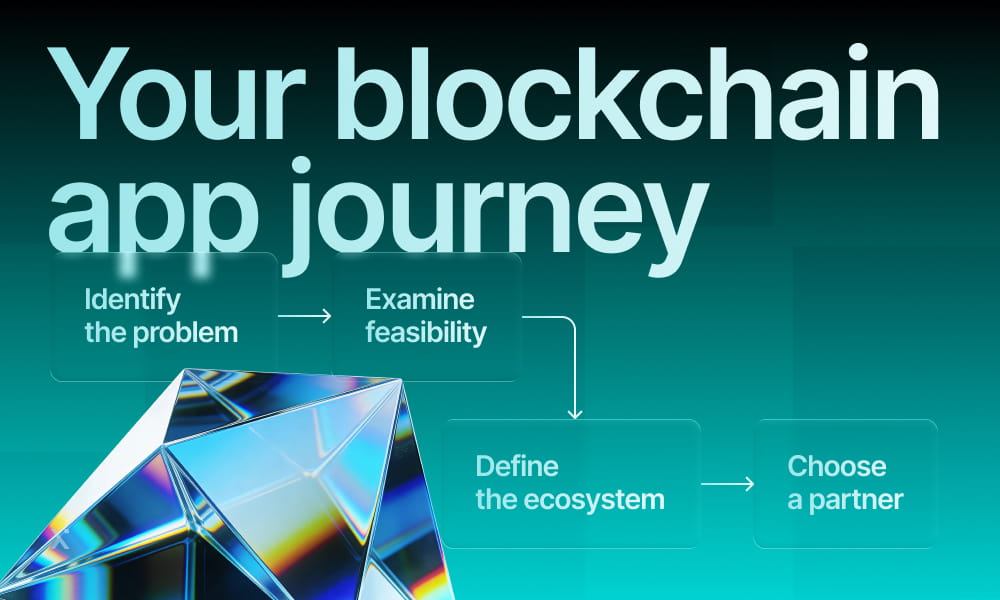

Where to begin your blockchain app journey

When you decide to invest in fintech blockchain software development, it’s important to follow a consistent roadmap that begins with defining the core problem and examining technical feasibility. Depending on your goals, you might opt for a private ledger for internal security or pursue public blockchain development if your Fintech solution requires a global user base. You should analyze process fit, ROI potential, and regulatory implications.

These early product and architecture decisions are also a primary driver of cryptocurrency exchange development cost, especially if your roadmap includes trading or exchange functionality. Besides, the type of blockchain is crucial. If your project requires strict access controls and high transaction throughput, partnering with an experienced private blockchain development company can help you architect a permissioned network that meets institutional standards.

Let’s look at the types of blockchain and how they enforce blockchain fintech app development.

| Blockchain | Key benefits for fintech apps |

| Ethereum | Established ecosystem: largest network for DeFi and smart contracts. High interoperability: extensive developer tools, standards (ERC-20, ERC-721), and composability. |

| Hyperledger Fabric | Enterprise-grade privacy: permissioned network ideal for confidential B2B processes (trade finance, banking). Modular architecture: flexible consensus and data privacy models. |

| R3 Corda | Finance-specific design: built for financial agreements; unique “point-to-point” ledger. Legal compliance: integrates with legal prose and traditional systems. |

| Solana | High throughput & low cost: processes thousands of transactions per second with minimal fees. Scalability: suited for high-frequency applications like payments and trading. |

| Stellar | Efficient cross-border payments: specialized in fast, low-cost fiat and asset transfers. Built-in decentralized exchange: facilitates multi-currency transactions. |

| Binance Smart Chain (BSC) | Cost-effective & fast: lower fees and high speed, compatible with Ethereum tooling (EVM). Large user base: access to a major crypto exchange ecosystem. |

After selecting the blockchain, decide which features your app needs. A software partner should first help you define core user-facing features based on your business model. They might include:

- Digital wallet and secure identity management.

- Dashboard for tokenized assets and investments.

- Tools for creating and issuing digital securities.

- Peer-to-peer trading and payment channels.

- Automated smart contract agreements (e.g., for lending).

- Crypto payment gateway development services (if you are planning to build a comprehensive financial platform).

To build these, your partner will architect solutions using:

- Smart contracts. These are self-executing programs stored on the blockchain that automatically enforce the terms of an agreement, such as releasing a loan once collateral is locked.

- Asset tokenization standards. These are established technical rules (like ERC-20) that define how a real-world asset is represented as a digital token on the blockchain, ensuring compatibility across platforms.

- Secure consensus mechanisms. This refers to the protocol (e.g., Proof-of-Stake) that all network participants use to validate transactions and agree on the ledger’s state. It prevents fraud and ensures security without a central authority.

- Cross-chain bridges for interoperability. These are specialized protocols that enable the secure transfer of data and assets between different blockchain networks. As a result, your app operates across multiple ecosystems.

- API integrations for oracles and banking services. Oracles are services that connect smart contracts to external, real-world data (like market prices), while banking APIs are needed to link traditional fiat currency systems with your blockchain application.

The Intelligent Bank: Moving Beyond Automation to Strategic AI

Blockchain in Payment Services: Trends, Technologies, and Development Best Practices

What Is Stellar Blockchain and What’s So Special About It?

Blockchain fintech app development process

- Discovery & design: At this step, blockchain partners discuss the vision and the business logic. They usually touch upon formalization, smart contract architecture, consensus mechanism selection, and UI/UX wireframing.

- Prototyping & MVP: Building core smart contracts, developing a minimal front-end, testing on a testnet (e.g., Sepolia, Mumbai).

- Full development & integration: Backend development, integration with existing systems (APIs, legacy databases), advanced front-end.

- Rigorous testing & audit: Security audits (critical for smart contracts), penetration testing, performance load testing.

- Deployment & maintenance: Mainnet deployment, node management, ongoing upgrades, and user support.

As for the timeline, here are approximate periods required for each phase:

| Phase | Approximate timeline |

| Phase 1: Discovery & design | 3 – 8 weeks |

| Phase 2: Prototyping & MVP | 6 – 14 weeks |

| Phase 3: Full development & integration | 12 – 24 weeks |

| Phase 4: Rigorous testing & audit | Ongoing & 4-8 weeks (core audit) |

| Phase 5: Deployment & maintenance | 2 – 4 weeks (launch) + ongoing |

Every process has its pros and cons. The blockchain fintech application development involves distinct challenges. These primarily include scalability limitations, an uncertain regulatory landscape, and significant integration and security concerns.

To address these challenges effectively, a software development partner must implement specific, proactive measures. This includes adopting the latest consensus mechanisms and Layer 2 solutions to improve performance, actively engaging with legal experts and regulatory bodies to navigate compliance, developing robust middleware for smooth system integration, and conducting rigorous, regular security and smart contract audits. In general, a competent and experienced partner will leverage this expertise to help you avoid these common pitfalls and achieve the best possible result in the most efficient timeframe.

The Opportunities of Banking in Metaverse: What Companies Must Know to Stay Competitive

Crypto Payment Gateway: Costs, Benefits, Implementation

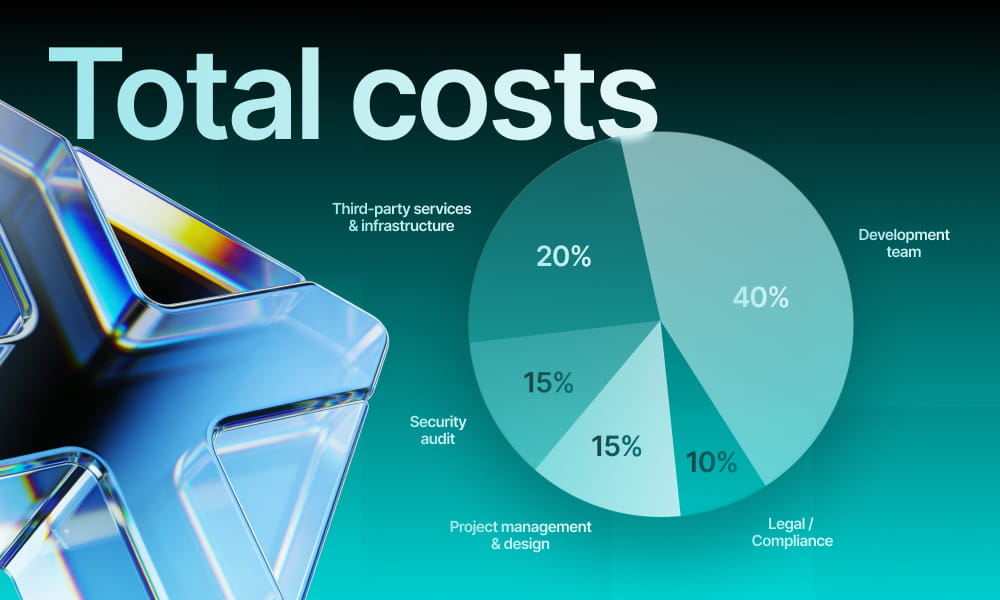

Understanding the cost structure

As far as the investment is concerned, there are key cost drivers that include:

- Project complexity: a simple payment gateway is cheaper than a full-scale tokenization platform, as the latter demands asset legal structuring, complex smart contracts, and regulatory compliance. Similarly, Web3 mobile app development introduces additional considerations such as wallet integration, seed phrase management, and smooth on-chain interactions, all of which add to the scope but are essential for user-facing blockchain products.

- Blockchain choice & consensus: for example, Ethereum has high developer availability but ongoing “gas” fees. Hyperledger Fabric requires specialized (often pricier) enterprise developers, while a custom chain has the highest initial development cost.

- Team composition: senior blockchain developers, smart contract auditors, and fintech domain experts are usually more expensive than mid-level specialists. However, this is non-negotiable for security and regulatory adherence, as cutting corners here is the most expensive mistake.

- Third-party costs: cloud infrastructure, security audit fees, legal/compliance consulting. These are often underestimated, yet critical for fintech products.

- Ongoing costs: these include network fees (gas), node maintenance, and team support.

Here are the approximate costs of developing various kinds of solutions:

| Project type / scope | Key characteristics | Approximate cost range (USD) |

| Proof of Concept (PoC) | Basic smart contract functionality, single feature, private testnet | $25,000 – $70,000 |

| Mid-complexity platform | Multi-feature (e.g., payments + tokens), custom smart contracts; integrations with 1-2 external APIs (KYC, oracles), professional UI/UX | $150,000 – $350,000 |

| Enterprise-grade solution | Full-scale platform (e.g., trading, lending, tokenization), high-security, audited architecture, complex integrations (banks, legacy systems), regulatory compliance focus, dedicated dashboard | $350,000 – $800,000+ |

Besides, the costs also depend on the location of your potential software development partner. For example, engineers’ rates from North America are higher than those from Eastern Europe or Asia. Here are approximate costs:

| Location | Approximate rate range (USD) |

| North America / Western Europe (in-house) | $180,000 – $300,000+ (annual per dev) |

| North America / Western Europe (agency) | $150 – $300+ / hour |

| Eastern Europe (Ukraine, Poland, Romania) | $50 – $100 / hour |

| Latin America (Brazil, Argentina) | $40 – $80 / hour |

| Asia (India, Philippines) | $25 – $60 / hour |

| Global platforms (freelance, e.g., Upwork) | $50 – $120 / hour |

MVP development services come in handy in reducing costs. A lean and focused MVP instead of a full-scale platform allows for developing only the core functionality. Besides, choosing the most efficient blockchain technology for your specific needs also helps to avoid custom builds when possible. Engaging a smart contract auditor early in development is also critical, as fixing a security flaw pre-launch is far cheaper than addressing a breach later.

Why PixelPlex is your ideal strategic technology partner

We have been dealing with blockchain and Web3 development services for almost 20 years already. Our portfolio features cryptocurrency development solutions for both high-growth startups and leading global enterprises. PixelPlex experts know how to transform intricate blockchain theory into intuitive, practical applications.

One of our core strengths is our “consultative engineering” methodology. We engage in a strategic discussion for each project to define and achieve superior outcomes. Our expertise spans the full spectrum of development, from constructing bespoke base-layer protocols to developing sophisticated networks of automated contracts. Below are some of our recent successful projects that illustrate this expertise.

| Solution | Features | Results |

| ERC-20 token platform | Multiple pools for token allocations, vesting, pause functions for security | ERC-20 token for all ecosystem operations with a total supply of 1,000,000,000 |

| Canton Network non-custodial wallet | Fast and secure authorisation, transaction history, and real-time alerts. | Top 10 position on the Canton Coin Validator Leaderboard |

| Web3 Antivirus | Smart contract analysis, transaction simulation, risk reports | Around 800,000 analyzed user transactions and 16,000 registered users |

Conclusion

Blockchain fintech application development assists businesses in building efficient, transparent, and secure financial services. As we have mentioned in our detailed overview, blockchain applications are diverse, and this technology is capable of addressing clear pain points in trade finance, payments, capital markets, and compliance. The journey from ideation to a live application involves strategic choices regarding technology, features, and partnership. While challenges like scalability and regulation exist, they are navigable with expert guidance. For forward-looking financial enterprises, blockchain is a technology that will bring a tangible competitive advantage.

FAQ

First of all, you should pay attention to their portfolio to decide if their expertise matches your expectations. For example, if you’re seeking to build high-performance decentralized applications, reviewing their experience with Solana blockchain app development is particularly important. Second, you should look for testimonials of real clients. You can examine Clutch rating or other similar listing platforms. Besides, you can arrange a meeting to ask questions regarding the blockchain fintech app development process of a particular company. While finding a truly reliable firm requires diligence, the right partnership is an investment that delivers both a product and a foundational advantage for your business.

Absolutely. Integrating AI is a powerful way to enhance a blockchain app’s capabilities. Our team at PixelPlex builds intelligent features like predictive fraud models, automated risk assessment, and smart contract optimizers that add a critical layer of efficiency and security, turning data into a competitive advantage.

First, the tokenization of RWAs (bonds, real estate assets) is happening. Second, cryptocurrencies will be more widely used for fast and secure transactions. Besides, blockchain is beneficial for financial institutions as it allows them to save costs on intermediaries and eliminate payment delays. Such an opportunity will push more companies to implement blockchain. Finally, as with any other sector, AI technology will continue to penetrate the financial sector and blend with blockchain.

Yes, you can. At PixelPlex, we discuss your vision during the discovery phase and suggest solutions. Blockchain integration is a feasible and popular request among our clients. For example, among our clients are those who require travel software development services for their existing payment platforms. We develop solutions that integrate smoothly and improve performance from day one.

Yes, through conscious design. The environmental impact of a blockchain is dictated by its consensus mechanism. At PixelPlex, we prioritize energy-efficient protocols like Proof-of-Stake and design custom solutions that minimize carbon footprint. Our work on the HELO Blockchain, for instance, demonstrates how scalable platforms can align with sustainability goals.

Divergent national regulations create a primary friction point for scaling blockchain finance. They force services to fragment operations, building custom compliance modules for each jurisdiction instead of a single, global protocol. This increases cost and complexity, directly hindering scalability.

For compliance, the effect is twofold. It creates a heavy, variable burden—navigating strict licensing in one country while operating in a regulatory gray area in another. This uncertainty is a major barrier to institutional adoption.