Big data analytics in banking is opening up new insights and driving major advancements. But what are the actual benefits and opportunities that the technology brings and what hurdles could come along with it?

Big data is making waves across industries and banking is no different.

With big data analytics in banking expected to reach $12.89 billion by 2031, FinTech and banking organizations are buzzing about the potential improvements this technology could offer.

In this article, we will delve into what big data analytics in banking really means, explore its applications and benefits, and discuss the challenges you should keep in mind before diving in.

Discover 50 key big data statistics and trends that show how big data is making a real impact across various industries and sectors

Why is big data analytics in banking so important?

Big data analytics in banking brings a whole range of perks that can boost growth and make services better. Essentially, data analytics services for the fintech industry are transforming how banks operate and compete.

Let’s take a closer look at some of the key advantages of big data in banking.

More personalized customer experience

Big data analytics services help banks and financial businesses get to know their customers on a whole new level.

With this tech, they can create more personalized products, predict what customers might need next, and provide recommendations that really hit the mark, which makes every interaction feel more meaningful, personalized, and engaging for customers.

Improved operational efficiency

Big data analytics helps banks streamline their workflows and pinpoint inefficiencies, which leads to smoother and much more efficient operations across the board.

Even better, reports show that financial companies effectively using big data have boosted their operating margins by over 60%, all while delivering better service to their customers. Thus, it is a win-win for both the business and the people they serve.

Ability to spot market trends early on

To stay ahead of the competition, banks must stay alert to market changes.

Big data provides the insights they need to recognize trends and understand customer behavior. For example, by analyzing past data along with current market signals, banks can spot a growing demand for digital services.

With these insights, they can tweak their strategies on the go, launch new products, or refine their marketing — all to meet customer needs before those needs even surface.

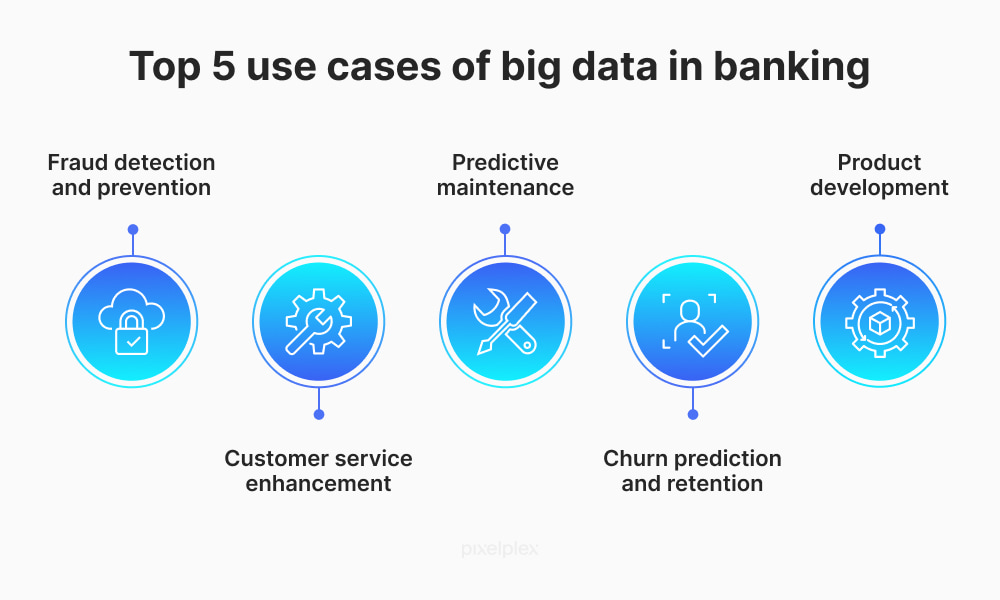

What are the main use cases and applications of big data analytics in banking?

Big data is being used in all kinds of ways in banking, from spotting fraud and managing risks to breaking customers into segments and predicting who might leave.

Now, let’s check out all the ways big data in banking is making a difference.

Fraud detection and prevention

In 2022, fraud losses in U.S. bank payments amounted to almost $1.6 billion. With advanced algorithms that track transaction patterns in real time, banks can catch unusual activity that might hint at fraud before it even happens.

For instance, the technology can detect red flags like a sudden large withdrawal from a different city or multiple quick purchases that could indicate something fishy.

Check out our machine learning fraud detection services and learn how our team is helping businesses bolster their security frameworks

Customer service enhancement

Banks are getting pretty good at understanding their customers — and a big part of that success comes from big data analytics.

By examining how different segments of customers spend, save, and invest, they can customize their offerings to meet specific needs. This means that instead of bombarding everyone with the same generic promotions, banks can send personalized offers that resonate with each customer’s lifestyle and preferences.

Advanced algorithms analyze patterns within customer segments, like young professionals, families, or retirees, which allows banks to craft targeted marketing strategies. Whether it’s a customized savings plan, investment opportunities, or exclusive rewards, these bespoke offers feel more relevant and personalized and enhance the overall banking experience.

Predictive maintenance

You might not think about the technology that keeps your bank running smoothly — but in fact big data is one of those vital tools needed for catching potential issues before they blow up.

Banks use data analytics and machine learning solutions to monitor their systems around the clock, looking for unusual patterns that could indicate a server crash or software malfunction. Considering that the median cost of unplanned downtime across 11 industries is around $125,000 per hour, the ability to prevent disruptions is not just beneficial, it’s essential for minimizing financial losses and ensuring seamless operations.

For example, during busy times like holiday sales, a sudden spike in transactions could overwhelm the system. In these cases, big data helps banks anticipate potential overloads by reallocating resources effectively.

On top of this, smart monitoring tools continuously track software performance and alert the tech team to any anomalies, thus enabling quick fixes that prevent disruptions to your banking experience.

Churn prediction and retention

The median churn rate for financial services businesses was found to be 19%. This figure highlights a persistent issue in the industry, as many banks and financial services companies have long struggled with a reputation for poor understanding of customer experience, which contributes to higher churn rates.

With the help of big data analytics, banks can track various customer behaviors such as how often clients use their services, the types of transactions they make, and even their interactions with customer support. If there is a noticeable drop in activity or signs of dissatisfaction, they can catch those signals early on.

Product development

FinTech and banking businesses are always looking to innovate and create new products that would meet customer needs and requirements. Thanks to big data, they now have powerful tools to spot trends and gather direct feedback in more meaningful ways. By sifting through data from sources like social media, surveys, and transaction histories, banks gain valuable insights into what people are really looking for.

For example, advanced analytics can reveal patterns in spending behavior and show which services are gaining popularity and which ones might be falling behind. If they see a growing demand for mobile banking features or personalized savings plans, they can quickly adjust to meet those needs.

On top of that, with machine learning solutions and natural language processing tools, banks can dive into online reviews and social media comments to get a better sense of how customers feel about their products. This helps them spot areas that need improvement or uncover gaps in their services that people want to see addressed.

Blockchain in Mobile App Security

Blockchain in Energy: Key Benefits and Use Cases

How to implement big data in banking in 5 steps?

While implementing big data analytics looks different for every business, there are a few universal steps that banks and FinTech companies can follow.

1. Collecting data

Banks gather data from multiple sources, including but not limited to transaction records, app and website interactions, and external feeds like market trends and social media. Once they have pulled all this information together, they will be able to form a detailed view of customer behavior, spot market shifts, and identify both risks and opportunities.

2. Cleaning and organizing data

After gathering all that information, the data gets scrubbed for accuracy.

Outdated, irrelevant, or incorrect data is removed and the rest is structured into a usable format, which is critical for any meaningful analysis and smooth processing.

3. Analyzing data

With clean and organized data, advanced analytics take over. Machine learning algorithms uncover patterns in spending habits, flag unusual transactions that could signal fraud, and reveal broader trends. The deep analysis helps banks understand both their customers’ behaviors and their overall business health.

4. Working with the insights gained

Once they have the necessary insights, banks use the help of a trusted predictive analytics company to forecast future behaviors. From identifying which customers might default on loans to predicting demand for new products, they rely on machine learning algorithms to spot emerging trends and possible security threats.

To enhance the use of these insights, banks can integrate predictive analytics with several advanced tools. For example, interactive dashboards provide customizable, real-time insights, while dynamic charts allow for multi-dimensional, filterable data views. In many cases, this integration is implemented through custom banking software development, ensuring analytics solutions align with existing banking workflows and security requirements.

For seamless analysis, banks can also leverage analytics API integration, such as TradingView or Google Analytics and real-time data sync for automatic updates and live data integration. Data export options, like CSV, Excel, or PDF, make sharing insights simple, while predictive analytics tools facilitate forecasting and trend identification.

5. Taking action

Finally, armed with these predictions, banks take proactive steps. Whether it is launching targeted financial products, fine-tuning customer service, or strategically investing in new areas, they use data to make informed and forward-thinking moves that improve customer experience and business performance.

Check out our transaction monitoring software and let’s have a chat about how we can assist you in enhancing your security and compliance

Challenges to be aware of before implementing big data in banking processes

Embracing big data in banking can indeed transform how institutions operate but it is not without its challenges. Banks and FinTech companies often encounter challenges that can slow down their ability to tap into this powerful resource.

Let’s dive into some of the key challenges they face and offer practical tips on how to overcome them.

Data security and changing regulations

With so much sensitive information in their hands, banks must prioritize data privacy. Customers are understandably concerned about how their data is managed and a single security breach can severely damage trust.

To maintain and rebuild that trust, banks need to stay compliant with regulations, including AML and KYC, and implement robust security measures to protect customer data at every step. This includes using encryption to secure data both in transit and at rest, multi-factor authentication to verify user identities, regular security audits to spot potential weaknesses, and advanced threat detection systems to monitor for any suspicious activity.

Data quality and accuracy

Poor-quality data can lead to misguided conclusions and poor decisions. That’s why banks should prioritize creating strong processes for regularly cleaning and verifying their data. This way, they can be confident they are working with the most reliable information available.

Integration with existing systems

Many banks rely on older systems that do not always mesh well with new big data technologies, thus complicating implementation and slowing down progress.

To overcome this challenge, banks can actively seek ways to integrate these legacy systems with modern technologies. By doing so, they can effectively bridge the gap, unlock the full potential of big data, and boost their operational efficiency.

Talent and expertise

Banks frequently encounter challenges in finding or developing talent with the right mix of data analytics skills and industry expertise.

To address this issue, they should consider forming partnerships with experienced tech providers specializing in big data analytics. By entrusting the complex tasks of data analysis to these experts, banks can tap into advanced tools and insights without the hassle of hiring and training new staff. Plus, this allows them to focus on their core mission — serving their customers while effectively harnessing the power of big data.

Cultural resistance

Implementing big data strategies often requires a shift in the organization’s mindset, which can lead to some hesitation among team members.

To ease this transition, banks can cultivate a culture that values data-driven insights and encourages openness to new approaches. Hosting data workshops and highlighting the benefits of big data can create an environment where change is embraced. This way, everyone feels more comfortable adapting to innovative practices and the transition gets smoother and more collaborative.

How to Hire a Blockchain Development Team: Top 10 Facts to Consider

How to integrate blockchain into your existing business infrastructure

Blockchain for Digital Identity: Overview, Guide & Facts

What does the future of big data in banking look like?

Big data analytics can exert a positive impact on a range of banking processes. Banks that embrace big data will be in a much better position to tackle their challenges and innovate their services, all while creating a safer and more satisfying environment for everyone. Customers, for their part, can look forward to more personalized experiences, enhanced protection of their personal data, and exciting new products that meet their needs.

If you are ready to explore how big data can elevate your banking processes, our big data services are exactly what you need. From consulting and engineering to architecture, QA software testing services, governance, and security, we cover it all.

Our team offers a wide range of data-related services, including data visualization, business intelligence, and data science engineering services.

We also provide a whole suite of FinTech and banking services to tackle any financial challenge you might face. With expertise in blockchain, DeFi, AI/ML, data analysis, security, and tokenization, we are excited to team up with you and create solutions that feel just right for your needs.

Ready to hand over your challenges to us? Let’s chat and see how we can make a real difference for you.