The financial sector is presently at the forefront of a digital revolution, ushering in transformative trends that are reshaping the experiences of both financial institutions and their clientele.

The financial services industry is undergoing a seismic shift fueled by digital transformation. Industry reports project that the global market for digital transformation in financial services is set to soar to a staggering $164.08 billion by 2027. This evolution is driving a new era of efficiency and customer-centricity, positioning technology not merely as a tool, but as a core business enabler.

In this digitally-charged environment, two factors are particularly influential: the widespread adoption of smart devices and increasing global connectivity. These are giving rise to key technological trends that are proving to be game-changers in the sector. Today’s consumers, equipped with a multitude of digital tools, are increasingly favoring financial institutions that are both tech-savvy and forward-thinking, especially those that are leading the charge in adopting these pivotal trends.

So, what exactly are these transformative trends in the realm of financial services? How are they altering the ways in which financial institutions operate and meet customer needs?

In this article, we delve into these critical questions and explore the top trends currently shaping the financial services landscape.

Explore the top 10 trends that are set to shape the future of FinTech

Top 6 digital transformation trends in financial services in 2023 and beyond

When diving into digital transformation, financial organizations are following industry-specific trends. The most popular ones include digitization, automation, greater cooperation , the introduction of new payment methods, improved use of data, and new approaches to user experience.

1. Digitization

Today’s financial consumers, equipped with digital devices and a preference for online interactions, expect their banking and financial services to be as seamless as their favorite apps. This pressing demand is compelling institutions to redefine traditional banking models and processes into sophisticated digital counterparts.

Financial applications and platforms that are digitized and optimized offer tailored services, ranging from real-time transaction alerts to personalized investment advice using AI-driven insights. These digital advancements play a pivotal role in enhancing customer satisfaction, fostering trust, and securing loyalty in an industry where trust is paramount.

But digitization in finance goes beyond just online banking or mobile apps. It’s about leveraging technologies like blockchain for secure transactions, employing big data analytics to predict market trends, and utilizing AI for fraud detection. Moreover, with the rise of fintech startups, traditional banks and financial institutions find themselves in an era of collaboration, merging legacy systems with innovative solutions.

In an increasingly competitive financial landscape, those who fully embrace digitization set themselves apart, gaining an edge in efficiency, security, and customer experience. Institutions that prioritize this digital shift are not only catering to current demands but also future-proofing their operations against upcoming industry evolutions.

Kickstarting your business's digital transformation? Explore our guide to sidestep 7 common challenges

2. Automation

Financial companies are dealing with more data and transactions than ever before. Doing things the old way, with people manually entering data and processing tasks, is slow and can lead to mistakes. That’s why automation is becoming a hot trend in the finance world.

By using automation, companies can get a lot of work done quickly and with fewer errors. This means that customers can trust these companies more, and it also gives these businesses a leg up over competitors who are slower to adopt new tech.

Tools like AI and RPA are leading the way in making these changes happen. AI can help with things like spotting unusual activity in accounts, which could mean someone is trying to commit fraud. RPA, for its part, takes over repetitive tasks, like sorting through data, so that employees can focus on more important things.

But it’s not all smooth sailing. Companies have to think about issues like keeping customer data safe and making sure new tech works with their old systems.

But even so, the trend is clear: automation is the future of the finance industry, and companies that get on board stand to benefit the most.

3. Greater cooperation for technological advancement

To stay abreast of the accelerating pace of technological innovation, financial institutions are increasingly forming partnerships with fintech companies. These alliances leverage the unique strengths of each partner — whether it’s the technological expertise of fintechs in areas like enterprise blockchain development and AI or the expansive customer base of traditional financial institutions.

Such strategic collaborations offer multiple advantages, including market expansion, brand development, and the exploration of new application domains like cybersecurity and risk management.

However, these partnerships also come with their own set of challenges, such as the need for seamless integration of different technology platforms and compliance with data privacy standards. By navigating these complexities successfully, both traditional banks and disruptive fintech firms can preempt market shifts, create unparalleled customer value, and solidify their positions as industry leaders.

4. New payment methods

As the momentum of online payments continues to accelerate, there’s a pressing need for more sophisticated, reliable payment services. The industry is being propelled by user demands for speed, unparalleled security, and the utmost convenience. Cutting-edge technologies like contactless payments, biometric verifications, and blockchain-based solutions are emerging as responses to these needs.

Industry giants like PayPal, Apple Pay, and Google Pay dominate the digital payment landscape. For instance, in 2022, Apple Pay reported a user base of over 507 million, underscoring the immense trust consumers vest in established digital payment platforms that seamlessly integrate these advanced technologies.

As we delve deeper into the digital age, the horizon of online payment methods will continue to expand. The industry is poised to introduce more groundbreaking solutions, each tailored to cater to the evolving and diverse requirements of a global audience.

Check out our detailed guide to embedded finance and see how your business can use it

5. Improved use of data

Improved use of data is more than just a business trend — it’s an imperative in our digital age. The modern landscape of data collection and analysis, fueled by rapid advancements in big data technologies, machine learning, and AI, has the potential to redefine the corporate world. These advancements provide deep insights into consumer behaviors and preferences, enabling businesses to offer an unprecedented level of personalization.

Moreover, real-time data analysis through AI can significantly improve the immediacy of decision-making processes, allowing businesses to respond faster to market changes. However, successfully harnessing these technologies requires overcoming challenges such as data security, privacy concerns, and the integration of legacy systems.

The projected market size for business intelligence and analytics software, expected to touch $18 billion in 2025, underscores its increasing significance. This is not merely a testament to the technology’s potential but a clear indicator of businesses acknowledging the undeniable power of data-driven strategies. As this realization deepens, we can anticipate an even more significant surge in demand for state-of-the-art analytical tools.

Get insights into data-driven decision making and the benefits it offers

6. New approaches to design

The majority of financial companies already follow the three key design principles helping to gain customers’ engagement: simplicity, speed, and user-friendliness. These principles, when executed effectively, can drastically reduce friction points and foster trust between the institution and its clientele.

For instance, DBS Hong Kong stands out as a bank that ardently focuses on enhancing user experience. Their commitment is evident in their efforts to ensure smooth navigation and an intuitive design, all the while streamlining the performance of repetitive operations for their users.

Such approaches not only increase user satisfaction but also cultivate a sense of loyalty, with customers more likely to recommend and stick with services that prioritize their ease and convenience.

As digital interactions become the norm in the financial world, companies that consistently prioritize and innovate in UX design will undoubtedly set themselves apart, enjoying a prominent position in the ever-evolving landscape of customer preferences.

Well-thought UI/UX design is of utmost importance for a successful project. Check how PixelPlex designers can nail it

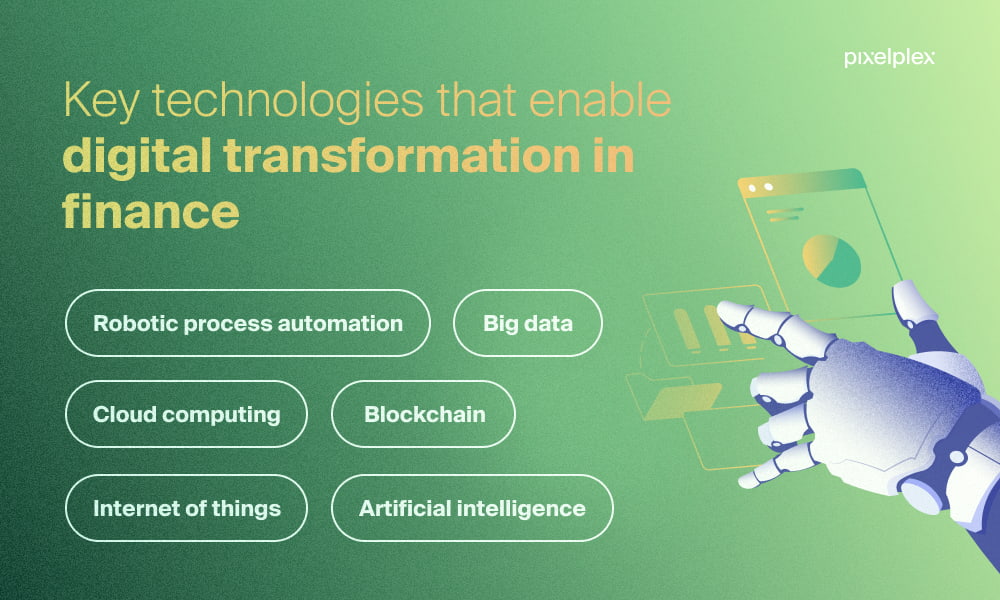

Which technologies drive digital transformation trends in finance?

Financial institutions looking for innovation have a variety of mind-blowing technologies to choose from. Robotic process automation, big data, cloud computing, blockchain, internet of things, artificial intelligence — these are the solutions that stand at the forefront of digital transformation.

Let’s examine their possibilities in detail.

Robotic process automation

Robotic process automation (RPA) is a technology that makes it easy to create and manage software robots that imitate human actions.

RPA in finance helps handle great volumes of standardized processes, leaving little room for errors and sparing humans from hours of monotonous work. It also reduces operational costs and speeds up customer service, delivering quick answers to the most frequently occurring problems and questions.

The technology is easily intertwined with existing systems, so it doesn’t require much effort or many resources to implement it. According to the statistics, around 80% of finance leaders already use RPA or are planning to introduce it to their workflow.

One of the banks leveraging RPA technology is Bank of America. Robots are primarily employed in customer service, regulatory compliance, and foreign money transactions. RPA was integrated into the existing infrastructure so no invasive actions were made to the bank’s systems.

Big data

It is predicted that by 2025 463 exabytes of data will be generated per day. It is simply impossible to analyze this amount of information relying on traditional approaches. So this is where big data steps in.

Big data is an umbrella term combining various instruments and methods for processing huge amounts of information. In banking and finance, this technology can be used to get valuable insights about customer behavior and demand, strengthen security measures, spot weak points in the current workflow and identify what works perfectly. Equipped with this knowledge, banks and financial institutions can significantly improve their processes and facilitate decision-making.

For example, big data technology helped Danske Bank combat fraudulent activities more effectively — detection has become 50% more accurate since big data implementation.

Don’t miss our article to acquire a better understanding of big data, data science, and data analytics

Cloud computing

Finance institutions process enormous quantities of information and this data needs reliable storage. As it is quite costly to maintain their own databases, financial companies turn to cloud technology — servers and storage space that exist on the internet.

Cloud computing makes it quick and easy to navigate through huge data storage, and also eliminates the need to spend money on special hardware and software and running on-site data centers. What’s more, cloud storage is highly reliable as it makes data backup and disaster recovery: 94% of companies report that their online security has improved with cloud computing.

A perfect example of cloud computing leveraged by a financial institution is the case of Starling Bank. The bank turned to BigQuery, one of the leading cloud computing providers, to glean valuable insights from the collected data and thus deliver the best customer service possible. Since Starling Bank generated £188 million in revenue in 2021, which is a 157%increase compared to 2020, we may conclude that this collaboration works pretty well.

Get amazed at how the finance sector stands to benefit from augmented reality technology

Blockchain

Blockchain development has already disrupted the world of finance with its cryptocurrencies and NFTs. But this technology has a lot more to offer — it’s not for nothing that the global blockchain in the financial services market is expected to reach $12.39 billion in 2026.

First of all, blockchain can greatly improve data and document management. Since everything that enters the chain stays there forever and is immutable, it is a great tool for maintaining verified documents. It means that different processes, from payments to loans, can be executed much faster, since there will be no need to re-collect and certify documents for every operation.

Blockchain can also contribute to the faster and more efficient execution of repetitive tasks such as compliance and regulatory reporting. By incorporating STO development, financial institutions can streamline token offerings while adhering to regulatory requirements. Smart contract development services can help automate operations, eliminating human error and ensuring that tasks like reporting are performed within a set timespan and in the correct order.

Furthermore, blockchain in payments allows transactions to be executed much faster through becoming a P2P operation involving no intermediaries. This can considerably enhance customer experience as everyone wants their money operations managed quickly.

In addition, finance organizations working with blockchain can collect digitized KYC and AML data as well as transaction history, which reduces the risk of fraud and enables real-time authentication.

Transform your journey with our expert financial software development and consulting services

Internet of things

A financial internet of things (IoT) device familiar to almost everyone is the automated teller machine (ATM). ATMs help to streamline real-time transactions, enabling people to carry out simple operations without the need to stand in long queues to speak to bank tellers. Modern machines have progressed significantly — some are even able to offer livestream video with support teams if a customer requires additional assistance.

Now financial organizations are diving deeper into IoT technology and uncovering its more sophisticated features. For example, some banks use beacons — tiny wireless transmitters that send Bluetooth signals to smart devices within reach. This way they drop special offers into clients’ smartphones or notify employees when a customer with special needs arrives at the bank so that they can provide prompt assistance.

TBC Bank is one of the banks that have successfully introduced beacons into their workflow. The new feature has helped them to enhance customer experience and level up awareness of the bank’s offers.

Banks can also invest in adding smart speaker features to their apps, allowing people to inquire about account balances and their latest transactions via voice instructions., For example, U.S. Bank installed a voice-based smart assistant in its mobile app. The assistant uses natural language processing technology to understand human speech.

https://pixelplex.io/services/internet-of-things/

Artificial intelligence

Artificial intelligence (AI) is an essential component of digital transformation in financial services. It is used by millions of clients all over the world in the form of virtual assistants and chatbot solutions. The global market for chatbots in banking, financial services, and insurance (BFSI) is expected to reach $7 billion in 2030.

In stark contrast to humans, chatbots can attend to customers’ questions 24/7 across a multichannel communication network. This helps employees to focus on more complex tasks and allows companies to maintain a smaller support team, consequently reducing expenses.

AI is also used to enhance customer identification and authentication and provide personalized insights and recommendations. In addition, the technology can anticipate risks, detect and prevent payments fraud, boost Anti-Money Laundering (AML) measures, and perform Know Your Customer (KYC) regulatory checks.

The largest US bank, JP Morgan, is actively using AI across its key processes, including fraud recognition and risk mitigation, natural language processing for virtual assistants, and client intelligence.

Not only AI: explore how machine learning can be used in anti-money laundering

How can your financial organization start its digital transformation and implement novel finance trends in its workflows?

There are several aspects you need to focus on while redesigning your financial business so that it reaps all the benefits of the new technologies:

Communicate your vision

Senior leadership should make sure employees understand the importance and goals of digital transformation, so that everyone works towards its successful implementation. Don’t forget to regularly highlight the benefits of this transition, to keep everyone motivated. Plus, be attentive to your employees’ suggestions and concerns throughout the process, so that you have first-hand knowledge of what is going on.

Emphasize training

To increase employee engagement in digital transformation, it is very important to invest in learning and training. This will not only help employees understand the technologies better but also reduce the stress associated with encountering something new.

Invest in cutting-edge digital tools

To streamline your business processes, automate workflows, and receive actionable insights, you should invest in such technologies as RPA, big data, IoT, etc. You need to create a digital workplace that is effective and interoperable — all databases, tools and applications should be easy to access.

Prioritize consumer experience

Your customer is your top priority, so make sure new technologies you implement are targeted to enhance clients’ experience. Focus on developing smooth and intuitive solutions, such as self-service banking portals.

Revamp existing systems and processes

To achieve great results from digital transformation, simply adding new technologies is not enough. You need to take time to upgrade already existing systems to achieve a mix of completely new and reformed processes to deliver best performance.

The future of digital transformation trend in financial services

Digital transformation of the financial sphere will gather pace with each passing year as companies and banks adopt digital transformation trends. It is no longer possible to ignore the rise of online banking and the overall shift towards conducting operations remotely rather than in physical locations.

Besides the actual communication with clients, new technologies such as RPA, big data, cloud computing, blockchain, IoT, and AI will streamline all vital aspects of banking and financial services, making both internal and external processes reliable and performant.

Thinking about bringing innovation to your business? Let the PixelPlex team assist you with this. Our custom software development company, backed by expert developers and seasoned consultants, offers actionable insights and tailored solutions to ensure your project truly stands out.

Contact us — and we will uncover the true potential of your business.