Blockchain has been transforming the payments landscape, offering unprecedented security, speed, and transparency and promising a future where every transaction is efficient, reliable, and most importantly, trustless.

The global blockchain market is experiencing robust growth, with projections suggesting it will reach $469.49 billion by 2030.

This technology has already made significant inroads into various business workflows and sectors, such as retail, supply chain, healthcare, and real estate. Additionally, blockchain is revolutionizing the worldwide payments ecosystem, guiding us toward a future characterized by heightened efficiency and transparency.

Read on to learn about blockchain in payments and explore the potential benefits it provides.

Unlock the potential of your business with our cutting-edge enterprise blockchain development services

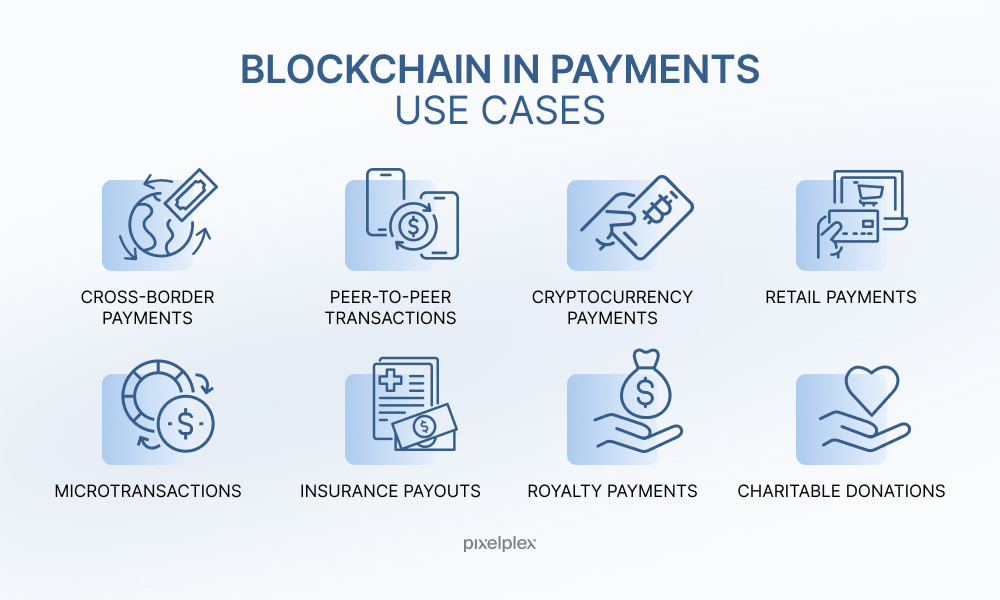

Top 8 use cases of blockchain in payments

Blockchain technology offers diverse applications in payments, paving the way for a new approach to conducting and processing transactions.

Below, we’ll delve into the eight most notable use cases of blockchain in payments.

1. Blockchain in cross-border payments

Sending money across borders using traditional methods can be slow and expensive due to various issues, such as currency exchange rates, processing fees, differences in time zones, and limited business hours, among others.

Blockchain, however, can provide a seamless solution to these pressing issues. Its decentralized system makes cross-border transactions swift and cost-effective. No intermediaries means no extra charges or delays, making it easy to transfer funds between countries. Plus, transactions happen almost instantly, which is perfect for today’s fast-paced global economy.

2. Blockchain in P2P payments

Through the decentralized blockchain network, individuals can carry out peer-to-peer (P2P) transactions, eliminating the need for intermediaries such as banks. This not only eradicates additional fees but also guarantees quicker and more efficient transfers. All users require is a reliable internet connection to send, receive, and transfer funds.

Every P2P transaction is documented on the blockchain in a tamper-resistant and transparent way, offering a verifiable track for all participants. The decentralized attribute of blockchain further bolsters security, making it an optimal solution for seamless, trustworthy transactions.

Step-by Step Guide to P2P Crypto Exchange Development

How to Develop a Peer-to-Peer Lending Application: PixelPlex’s Detailed Guide

Top 6 Stellar Blockchain Use Cases

3. Blockchain in cryptocurrency payments

Blockchain serves as the foundational technology in crypto payments, playing a vital role in maintaining transactional security and reliability. It applies cryptographic principles to authenticate transactions, embedding an additional layer of trust and integrity within digital payments.

Blockchain spreads transaction data across many computers, making crypto transactions resilient to single points of failure. This, along with advanced security measures used in blockchain, protects the data from tampering and authenticates transactions, improving the overall safety of the crypto payment solutions.

4. Blockchain in retail payments

Blockchain in retail payments offers benefits to both sellers and buyers.

Retailers get instant, fixed transaction records, which improves auditing and reduces fraud risks. Plus, using smart contracts, they can automate processes, like warranties and return policies, making operations more efficient.

Buyers, on the other hand, can enjoy clear and trackable transactions. They can also use blockchain-powered loyalty programs, which allows for innovative functions like exchanging tokens with other users or converting them into different rewards.

Blockchain in Payment Services: Trends, Technologies, and Development Best Practices

5. Blockchain in microtransactions

Microtransactions, or micropayments, are minor online financial transactions, typically involving sums of a few dollars or less. They are responsible for driving transactions for digital commodities in mobile apps, games, and various digital content.

Despite their significance, micropayments’ potential is often curtailed by high transaction fees and delayed processing in traditional systems. Luckily, blockchain technology presents a major upgrade by eliminating intermediaries and their subsequent fees. This not only accelerates transaction speed but also improves cost efficiency, thereby optimizing the overall micropayment experience. As a result, with lower costs and faster transactions, businesses can utilize micropayments more effectively, opening up new possibilities for digital commerce. Trusted cryptocurrency payment gateway development services would really help here.

6. Blockchain in charitable donations

Blockchain offers a novel method for charitable donations, promoting transparency, efficiency, and donor trust. Its unchangeable ledger enables donors to track their contributions in real time, validating their application and bolstering trust. Importantly, by employing decentralized identity solutions, blockchain also preserves donor anonymity, fostering increased donations.

The use of smart contracts also permits conditional giving, meaning that funds can be released only when predefined project objectives are achieved, which enhances accountability within the charitable sector.

Embrace the future of decentralized applications with our smart contract development services

7. Blockchain in insurance payouts

Traditional insurance payout procedures are typically slow and bureaucratic. However, blockchain technology can mitigate this by introducing decentralized transactions, eliminating the need for multiple intermediaries, and speeding up the process. Besides, blockchain in insurance can help verify and secure large amounts of data and ensures more robust fraud detection mechanisms, leading to more trustworthy claim assessments.

8. Blockchain in royalty payments

Utilizing blockchain in royalty payments offers transformative benefits to artists, creators, and publishers.

Typically, royalty payments involve complex distribution systems, often leading to discrepancies and delays. However, blockchain’s decentralized and transparent nature ensures direct, timely payments by accurately tracking content usage.

Moreover, the blockchain-enabled tokenization feature allows for the rights to a work to be tokenized, facilitating fractional ownership and introducing new revenue opportunities for creators.

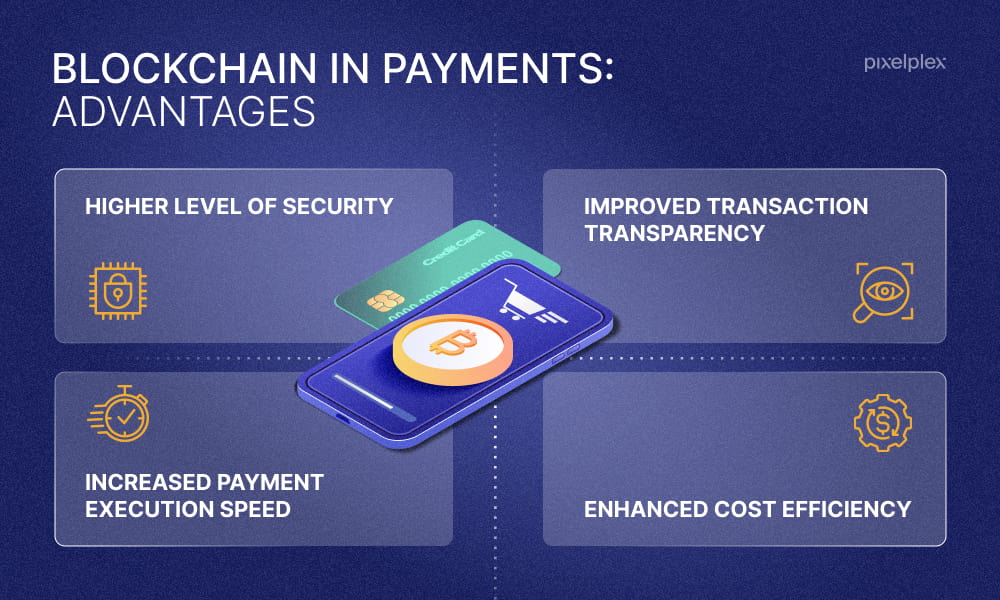

What are the benefits of using blockchain in payments?

Considering the aforementioned blockchain payment systems and solutions, it is clear that this technology offers numerous benefits. The most significant are a higher level of payment security, improved transaction transparency, increased speed of payment execution, and enhanced cost efficiency, typically achieved through modern payment software development that integrates blockchain infrastructure into real-world financial systems.

Higher level of security

The decentralized nature of blockchain allows transactions to be distributed throughout the decentralized network, making it enormously difficult to make changes in or tamper with transactions.

On top of this, blockchain employs advanced cryptography to enhance transaction security. Each transaction is encrypted using intricate algorithms, making them next to impossible to decipher without the correct keys.

Improved transaction transparency

Implementing blockchain in payments can create a trustless environment where financial transactions are transparent and easily verifiable. Consequently, this leaves no room for anyone to engage in corrupt practices or financial mismanagement without detection.

Increased payment execution speed

A key reason for incorporating blockchain in payment systems is its ability to rapidly process transactions, irrespective of the geographic locations of the involved parties.

Blockchain employs a decentralized network, circumventing traditional banking systems that often slow down international transactions. Its consensus mechanisms facilitate quick, direct transfers.

Enhanced cost efficiency

Blockchain operates on a decentralized network, where transactions are verified through consensus algorithms like Proof of Stake, Delegated Proof of Stake, Proof of Authority, and Proof of History. By bypassing traditional banking channels and their associated fees, blockchain not only streamlines the transaction process but also makes international transfers more cost-effective.

Crypto Payment Gateway: Costs, Benefits, Implementation

Custodial vs. Non-Custodial Wallet: Everything You Need To Know

Navigate the world of blockchain with confidence through our expert consulting services

5 steps on how to integrate blockchain in payments

Implementing blockchain in payment systems is a complex task that requires businesses to pay close attention to various details. In the following section, we will examine the critical steps necessary for successfully integrating blockchain into your payment processes.

Step 1. Define your project goals

First off, you will need to determine your specific business goals and needs and be able to fully understand how exactly blockchain can address them. This implies identifying the challenges in your current payment system that blockchain has the ability to solve, such as high transaction costs or long processing times.

It is also necessary to understand how the transparency and security features of blockchain can enhance your payment system and build trust among your users.

Step 2. Select a blockchain platform

In this stage, you have to execute thorough research into various blockchain platforms to identify the most suitable one for your blockchain payment system. Analyze and assess each platform’s core parameters such as scalability, security, transaction speed, community support, and its adaptability to future technological advancements.

Step 3. Think out the payment system’s functioning and user flow

Before starting the development process, make sure that you have outlined the functioning principles and mechanisms of your solution. You should map out how transactions will be initiated, validated, recorded, and verified within your blockchain.

Also, collaborate with UX/UI designers to provide an intuitive and user-friendly interface for your payment system. This will ensure that users can easily navigate and conduct transactions, improving overall customer experience.

Elevate your digital products with our captivating UX/UI design services

Step 4. Start the blockchain payment system development process

The blockchain payment system development process requires an experienced and skilled team. Therefore, you have to assemble a group of professionals, comprising blockchain developers and consultants, project managers, and business analysts, who are adept in blockchain technology, smart contracts, and secure coding practices.

In addition, ensure that the team is prepared to handle any regulatory and compliance aspects associated with creating a payment system.

Step 5. Test, deploy, and monitor the system

Before rolling out the solution, you need to carry out comprehensive quality assurance testing to detect and fix any bugs or security vulnerabilities. After deployment, continually monitor the system’s performance and user feedback in order to make necessary updates and enhancements.

Aspects to consider before implementing blockchain in payment systems

While incorporating blockchain in payments might seem intriguing and promising, businesses need to consider and thoroughly analyze several key factors before introducing this technology into their payment solution. These include the costs of implementation, user acceptance, compatibility with existing systems, and the need for additional security measures.

Blockchain implementation costs

Blockchain is rather expensive to implement, which is why you will be better off if you calculate and analyze the costs associated with its implementation before diving in.

An in-depth cost-benefit analysis can determine if the long-term benefits of adopting blockchain outweigh the initial investment, ensuring a strategic decision for the business’s future.

User acceptance

Although blockchain offers users many benefits, businesses still should estimate if their customers are ready to adopt the new, blockchain-based form of payment.

Consider carrying out customer surveys to gauge acceptance levels and tailor their rollout strategies accordingly. Plus, remember that the user interface plays a vital role in customer acceptance. That is why you need to ensure that your blockchain payment system is user-friendly and intuitive.

Compatibility with existing systems

It is essential to provide a smooth blockchain integration of a new payment system with existing legacy solutions to minimize disruption to current operations.

A seamless integration ensures that business operations remain efficient while offering users additional transaction options through blockchain. Rather than posing an obstacle, blockchain should complement and strengthen your workflows, enabling your organization to showcase improved performance.

Additional security measures

Businesses integrate blockchain in payment solutions to add an extra layer of security to transaction execution. However, it is crucial to realize that blockchain is not a panacea and it must be complemented with additional security measures to protect against potential risks such as user errors, wallet vulnerabilities, or cyber threats.

Top 10 Blockchain Use Cases In 2026: How Your Business Can Ride the Wave

Top 10 Blockchain Development Companies in 2026

Looking for a reliable blockchain protocol with the ability to handle high transaction throughput? Check out our TON development services

Closing thoughts

Blockchain is reshaping the payments landscape by providing secure, faster, more transparent, and cost-effective solutions. Its decentralized nature and the ability to optimize transactions have proven beneficial across all types of payments — from peer-to-peer to cross-border transactions.

If you are considering incorporating blockchain into your payment systems, PixelPlex blockchain development company can help you navigate this complex landscape.

With our expertise, we can design and implement a blockchain solution tailored to your specific business needs and requirements. We cover everything from crypto payment solutions and blockchain API implementation to peer-to-peer crypto exchange development.

Get in touch with us today and let’s transform the future of payments together.