Peer-to-peer lending apps have upended the way individuals borrow and lend money, helping them bypass traditional financial institutions and enjoy more direct, convenient, and user-centric alternatives.

The evolution of financial technology has ushered in a new era marked by agile transactions, with peer-to-peer lending apps leading the way.

P2P platforms, designed to connect borrowers and lenders directly, are more than just a passing trend. Recent statistical data underscores their importance: the global P2P lending market is projected to reach a valuation of $804.2 billion by 2030.

Considering this impressive growth forecast, developing a P2P lending app now could place businesses at the forefront of financial innovation and help them stay competitive.

Read on to learn more about lending software development, peer-to-peer applications, their advantages, and operational principles, and delve into the steps and strategies crucial for effective P2P lending app development.

What is a peer-to-peer lending app and how does it work?

A peer-to-peer (P2P) lending application serves as a digital platform that enables direct loans between individual borrowers and lenders, allowing all of the stakeholders involved to sidestep traditional banking systems.

By forging direct connections between borrowers and lenders, P2P lending apps present a streamlined alternative to conventional lending, catering to a wider range of participants.

A P2P app functions by letting borrowers outline their loan needs, while lenders choose and finance these requests. This process often involves credit evaluations, risk assessments, and interest rates set either by the platform or through a competitive bidding mechanism.

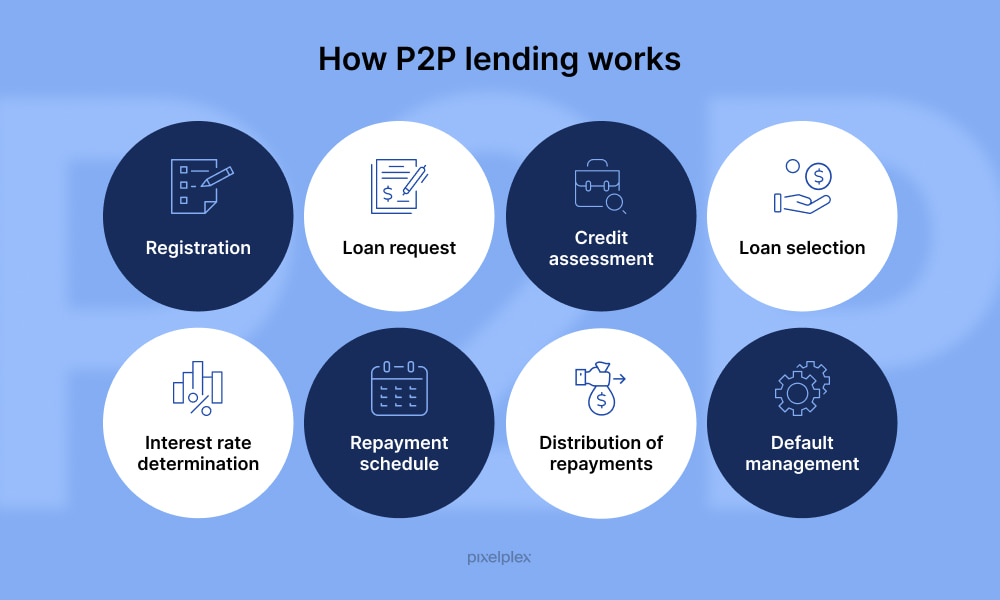

Here is a more concise breakdown of how a P2P lending application normally works:

- Borrowers and lenders sign up and submit essential details on the platform.

- Borrowers detail their loan needs, including the amount and purpose.

- The platform performs credit evaluations on borrowers, assigning a risk category or score to guide lenders.

- Lenders analyze available loans, deciding which ones to finance. They have the option to fund an entire loan or just a segment.

- Interest rates can be determined based on the borrower’s risk profile or via a bidding process among lenders.

- Borrowers adhere to the repayment schedule, which usually encompasses both the principal and interest.

- Lenders obtain repayments in line with their contribution, though the platform might subtract a service fee.

- In the event of loan defaults, the P2P platform manages the situation, which could entail collection actions or tapping into reserve funds.

Telemedicine App Development Explained: From First Ideas to Digital Health Solutions

PWA vs. Native Apps: Making the Right Choice

Curious about the future of FinTech? Dive in to discover the top 10 trends and stay ahead of the next big wave of innovations

How do P2P lending platforms differ from traditional loans?

Peer-to-peer lending and traditional loans primarily differ in their intermediaries and approval mechanisms. This difference is also a key factor when considering DeFi lending platform development.

P2P platforms establish direct links between individual borrowers and lenders, thus eliminating the need for conventional financial institutions. Leveraging technology, these platforms can swiftly assess risks, which makes them more inclusive for a diverse set of borrowers.

In contrast, traditional loans attract banks or credit unions as intermediaries and usually come with more rigorous approval criteria. While P2P lending offers avenues for individual investments, traditional loans confine this role exclusively to financial institutions.

What are the key advantages of P2P lending applications?

Peer-to-peer lending solutions offer a myriad of benefits, the most notable of which are quick execution speed, personalized financing options, enhanced transparency and visibility into financial processes, and more inclusive access.

Let’s take a closer look at each benefit.

Quick execution speed

Digital processes inherent to P2P lending platforms significantly streamline and expedite loan approvals and fund disbursements.

Compared to traditional banks, where procedures can extend over days or sometimes weeks, P2P applications typically finalize loans in a much shorter timeframe, often within a day or even less. This makes them a preferred option for borrowers with urgent financial needs and requirements.

Personalized financing options

P2P lending platforms offer a customized approach, which empowers borrowers to define loan amounts and choose repayment durations that align with their specific financial goals. This tailored control ensures a perfect match with individual liquidity needs and risk preferences.

Enhanced transparency & visibility into financial processes

On P2P lending platforms, terms, fees, and interest rates are clearly laid out from the start, thereby removing any ambiguity in loan conditions. This clear presentation not only keeps borrowers and lenders well-informed but also fosters trust within the lending platform.

As a result, provided with transparent and detailed information, users can confidently make more informed financial decisions.

More inclusive access

Mobile app development of P2P lending solutions broadens the scope of loan accessibility, catering to a diverse range of borrowers, including those with varied credit backgrounds. This inclusiveness removes traditional barriers and empowers users to access financial support and fulfill their specific monetary needs.

Blockchain in Mobile App Security: The Next-Gen Shield for Mobile Applications

PWA, React Native, Flutter or Native App Development — Which One Is Better?

Curious about how blockchain is transforming P2P transactions? Explore the top use cases in payments and see the technology in action

What are the limitations of P2P lending applications?

Despite their many advantages and capabilities, peer-to-peer lending solutions also come with certain limitations, including reduced safeguarding, increased default risk, potential fee implications, and the lack of regulation and oversight among others.

Reduced safeguarding

In P2P lending, loans often do not have the insurance you would normally find with regular bank deposits. This means both borrowers and lenders face more risks, especially if there is no backup plan for defaults or if the platform goes under.

Increased default risk

In the P2P lending ecosystem, there is an inherent risk associated with borrowers potentially failing to meet their repayment obligations.

Unlike traditional banks that have established risk mitigation strategies, some P2P platforms may have a higher susceptibility to borrower defaults, thus posing challenges for lenders expecting consistent returns on their investments.

Potential fee implications

Even though P2P lending apps can offer competitive rates, they sometimes levy service or origination fees. These additional costs, often hidden in the fine print, can erode the returns for lenders and inflate borrowing expenses, which might offset the perceived benefits of these platforms.

Lack of regulation and oversight

P2P lending platforms might not be as strictly regulated as traditional banks. This means they might not always adhere to the same standards or undergo rigorous compliance checks.

For users, this can lead to concerns about the platform’s stability, transparency, and fairness. As a result, without strong oversight, there exists a potential for unethical practices or mismanagement, which can put both lenders’ and borrowers’ funds at risk.

How to Develop a Fintech and Banking Platform: Our Detailed Guide

How to Revolutionize Retail With Computer Vision

Check out our blog article to discover how RegTech is revolutionizing compliance

What features should a peer-to-peer lending application include?

Each peer-to-peer lending application is unique, offering its own set of features that set it apart from other solutions in the market.

However, there are certain universal functionalities that every P2P platform should have to meet the needs of both lenders and borrowers and, crucially, to operate effectively.

Our R&D consulting team shortlisted the following core features and functionalities a P2P lending app should have:

- User registration and verification allows new users to sign up and undergo a secure identity verification process, ensuring the authenticity of both borrowers and lenders.

- E-payment integration acts as a unified payment gateway that streamlines transactions for both borrowing and lending activities.

- Pairing algorithms connect borrowers with suitable lenders by analyzing factors such as loan requirements, preferred interest rates, risk tolerance, and other criteria.

- Creditworthiness assessment tool examines a user’s financial data, debt-to-income ratio, transaction and payment history, and other relevant metrics to determine a credit score or rating.

- A centralized dashboard provides users with a snapshot of active loans, investments, and transaction histories, coming with analytics and adaptable features for a personalized financial overview.

- Automated notifications offer users real-time alerts for essential events like loan matches, funding updates, and upcoming repayment deadlines.

- User assistance interface helps users access a comprehensive help center, incorporating FAQs, tutorial guides, and direct support channels for quick resolutions and guidance.

- Document storage and management serves as a secure space within the app for users to upload, store, and organize crucial loan-related documents, ensuring both ease of use and safety.

- Transaction history overview presents a detailed log of all financial transactions needed for personal record-keeping and transparency both for lenders and borrowers.

- Built-in communication channels enable borrowers and lenders to communicate, clarify terms, or address concerns.

Exploring the Benefits and Impact of Blockchain Applications in Real Estate

Explore ECHO, a sophisticated blockchain protocol facilitating the decentralized economy

Why should businesses consider developing peer-to-peer lending apps?

Developing a peer-to-peer lending app is a smart move for businesses looking to tap into a fast-growing market.

P2P digital platforms are cost-effective and easy to scale, which means better profits and a leg up in the competitive world of finance. Plus, by adding advanced features, like smart credit checks using artificial intelligence or secure transactions with blockchain solutions, businesses can stand out and attract more customers and investors.

For fintech companies, creating a peer-to-peer lending app is also a great way to diversify their offerings. This not only boosts their brand but shows that they are keeping up with the latest trends. This forward-thinking approach can draw in more investors looking for fresh fintech solutions and skilled professionals wanting to work on new tech projects.

How to create a peer-to-peer lending app? PixelPlex’s step-by-step guide

Developing a peer-to-peer lending application is a challenging task that requires attention to many essential details.

In the following section, we will outline PixelPlex’s approach to creating a P2P lending application. Drawing on our extensive experience in the field, we will share valuable insights into what it takes to build a successful lending solution.

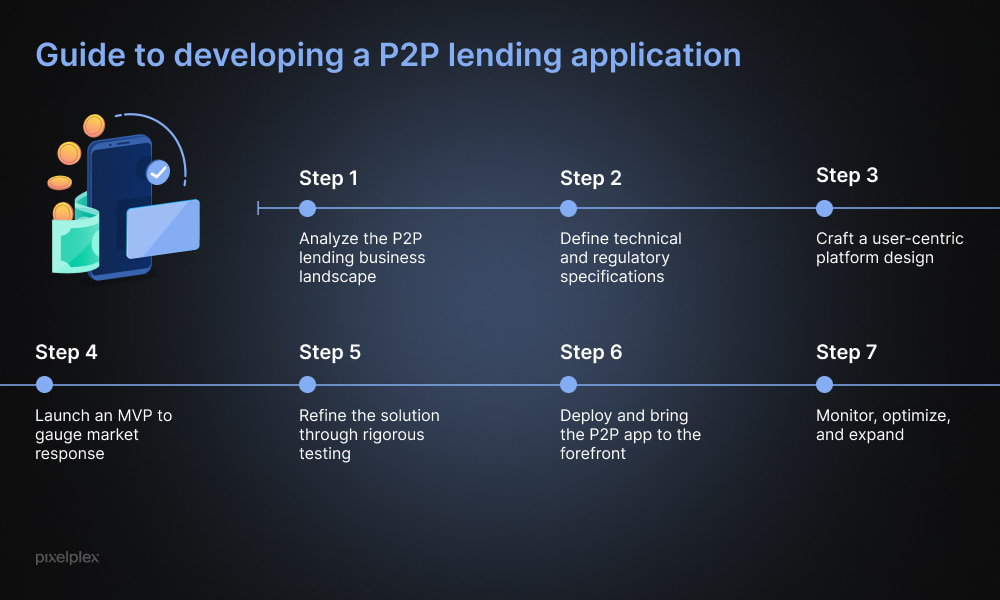

Step 1. Analyze the P2P lending business landscape

A well-conducted business analysis sets the stage for a strategic and informed entry into the P2P lending market.

Before laying the groundwork for a P2P lending app, you will need to thoroughly understand the current business landscape. This involves conducting a detailed study of prevailing market trends, identifying the most promising customer segments, and understanding effective revenue models.

By examining the strategies of top competitors, you may even spot potential market gaps and introduce your own unique vision. Such insights not only pinpoint areas of opportunity but also help tailor the app’s approach to deeply resonate with the intended audience.

Step 2. Define technical and regulatory specifications

This subsequent essential step involves aligning your P2P lending app with both the technical requirements and the regulatory standards of the financial industry. Attending to these technical and regulatory aspects from the beginning can greatly simplify the development process and reduce potential risks in the future.

Choose a robust backend framework capable of managing secure transactions and processing vast amounts of data. Then, outline the technical criteria for key features, such as credit evaluation algorithms, payment gateways, and encryption methods for data protection.

As well as this, acquaint yourself with both local and global financial regulations to ensure your P2P app adheres to all legal requirements, including those related to data privacy.

Step 3. Craft a user-centric platform design

The design of a P2P lending application extends beyond mere aesthetics — it serves as a pivotal tool for building trust, enhancing user retention, and elevating the overall user experience. The interface should be intuitive, guiding users seamlessly and minimizing the steps needed to complete tasks or access information.

Prioritize adaptive designs that accommodate various devices, utilizing both Android and iOS mobile app design and development services to maintain consistent functionality across mobile and desktop platforms. The platform’s visual identity should be infused with unique design elements that align with the app’s core goals and vision, all while streamlining user pathways.

What is more, the design of your solution should reflect the unique nuances of P2P lending, seamlessly integrating features like loan calculators, peer reviews, and transaction histories. By tailoring the interface specifically for P2P interactions, you will be able to cultivate trust and foster lasting user loyalty.

Bring your vision to life with our comprehensive UI/UX design services

Step 4. Launch an MVP to gauge market response

Introducing a Minimum Viable Product (MVP) acts as an initial market test. It allows businesses to showcase core features to a targeted audience.

By capturing real-time feedback from this preliminary launch, your business will be able to pinpoint areas for improvement and potential enhancements. These insights will also provide you with a deep understanding of user behavior, preferences, and the unique challenges associated with P2P lending.

Step 5. Refine the solution through rigorous testing

Upon harnessing initial feedback, the next phase involves executing comprehensive testing.

Dive into a suite of QA testing, from usability evaluations that ensure user-friendliness, to performance stress tests that ascertain the app’s resilience under peak loads.

In addition to this, given the sensitive nature of financial data in P2P lending, security tests are essential. As you uncover each glitch or potential enhancement, iterate and improve your solution.

By taking this meticulous approach to testing and refinement, you ensure your P2P lending app stands as a trusted, secure, and premier choice in the market.

Step 6. Deploy and bring the P2P app to the forefront

Transitioning from MVP to a full launch is an orchestrated effort that intertwines product deployment with strategic promotion.

After you have polished the P2P app’s features and made sure it is stable, it is time to release it to a wider audience.

Along with this, it is crucial to kick off a strong marketing campaign that will ensure that your app stands out, attracts more users, and grows in a competitive market. Using online ads, content marketing, and partnerships can help showcase what makes your app special and address common challenges in P2P lending.

Step 7. Monitor, optimize, and expand

As the P2P lending app integrates into the market, its success hinges on continuous monitoring and optimization.

Thereby, you will be better off if you deploy data analytics tools to scrutinize user behavior, loan transactions, and holistic platform performance. This will show you what users like, what they do not, and where improvements are needed. Based on this feedback, you can make necessary fixes and updates to keep the app fresh, relevant, and user-friendly.

As your P2P app gains traction, consider rewarding your users with special deals or bonuses for referring friends, keeping them engaged and loyal. To take things further, think about branching out into new areas or rolling out additional features. By doing this, you will not only enhance user experience but also solidify your app’s position in the competitive P2P lending landscape.

Overview of some of the top peer-to-peer lending apps in 2023

Peer-to-peer lending platforms have been experiencing increased popularity recently. Notable platforms in this evolving sector include Upstart, SoFi, Prosper, and Happy Money.

Let’s take a closer look at each of these platforms to understand what distinguishes them from the rest.

1. Upstart

Upstart is a lending platform that bridges consumers with a network of over 100 banks and credit unions, utilizing advanced artificial intelligence solutions and cloud applications to offer optimized credit products.

Catering to a broad spectrum of users, including those with fair to average credit, Upstart offers diverse loan types such as personal loans, automotive, small-dollar “relief” loans, and soon, home loans.

2. SoFi

SoFi is an online lending platform that offers a wide range of loan types, from debt consolidation to specialized needs like travel and more.

Alongside its diverse loan offerings, SoFi provides value-added services such as financial advising and unemployment protection.

Committed to propelling users towards financial independence, the platform ensures timely funds disbursement across all US states.

3. Prosper

Prosper, with its unique position in the lending marketplace, has facilitated loans totaling over $21 billion for more than 1.3 million borrowers. The platform stands out by enabling both individuals and institutions to invest, fostering a community-driven ecosystem of shared benefits.

Addressing a diverse range of needs, Prosper offers fixed-rate loans from $2,000 to $50,000, suitable for everything from home renovations to specialized green and military loans.

4. Happy Money

Happy Money has made a significant mark in the financial sector since its inception, facilitating over $5.2 billion in personal loans for more than 285,000 members. The platform is renowned for credit card debt consolidation, offering competitive APRs and unique benefits.

Beyond mere finance, Happy Money’s philosophy centers on leveraging money as a tool for happiness. By partnering with credit unions and community-focused lenders, the platform prioritizes its members, ensuring financial tools are both accessible and advantageous for everyone.

Closing thoughts

The development of a peer-to-peer lending app is a multifaceted endeavor that demands a strategic approach, from market analysis to technology selection and continuous optimization. However, the promise of high returns and the opportunity to establish a foothold in the rapidly expanding fintech sector makes it a worthy investment.

To ensure that your P2P lending app will thrive, you need to have the right partner to navigate the complexities of this development journey.

At PixelPlex, we offer specialized financial software development and consulting services tailored to bring your P2P lending app from concept to market successfully. Leveraging years of experience in delivering custom software development services and our deep technology expertise, we will help you build an application that not only meets but exceeds market expectations.

Contact PixelPlex today to take the next step in your fintech journey.

Disclaimer: The information provided in this article is intended for educational purposes only. It does not constitute advice or recommendations for developing, launching, or investing in peer-to-peer lending applications or their associated technologies. Please consult with qualified professionals before taking any financial or development risks.