Crypto investments can be lucrative, but the tax consequences can be a headache. Are you confident in your ability to navigate the complex world of crypto taxes?

The cryptocurrency market has experienced meteoric growth in recent years, captivating investors with its potential for substantial returns. A 2024 study by Statista found over 617 million global crypto users, highlighting the potential tax revenue at stake. However, the rapid evolution of this digital asset landscape has also introduced complexities when it comes to taxation.

This lack of confidence stems from the dynamic nature of the cryptocurrency market and the unique ways in which crypto income can be generated. While not all crypto activities are subject to taxation, understanding the nuances of US tax laws is crucial to avoid penalties and ensure compliance.

Our blockchain consulting company prepared a comprehensive guide on the crypto accounting and taxation system in the United States to help your business navigate the complexities and make informed decisions about your crypto operations.

Are all crypto transactions taxable?

While many investors believe all crypto transactions are taxable, this isn’t always the case. Understanding the nuances of US tax laws is essential to avoid penalties. Non-taxable crypto activities include:

- Acquiring crypto: Purchasing cryptocurrency with fiat currency (like cash) is generally tax-free.

- Holding crypto: Simply owning cryptocurrency without selling or trading it does not trigger tax liabilities.

- Donating crypto: Giving cryptocurrency to a qualified nonprofit organization is tax-deductible based on the asset’s fair market value at the time of the donation.

- Gifting or inheriting crypto: You can gift cryptocurrency to others up to the annual gift tax exclusion limit without incurring taxes.

- Wallet transferring: Moving cryptocurrency between your own wallets does not trigger tax events.

- Using crypto as collateral: Employing cryptocurrency as collateral for a loan is typically tax-free unless the lender takes possession of the asset.

The state of crypto regulations and laws in 2024 – discover in this article

How taxes on crypto work?

When you sell or exchange cryptocurrency for a profit, you’ll owe capital gains tax on the difference between your purchase price and selling price. This is similar to how you’d be taxed on the sale of stocks or real estate. For instance, if you bought Bitcoin at $10,000 and sold it some time months later for $12,000, you’d owe taxes on the $2,000 profit. As the crypto market grows, so does the need for crypto compliance solutions to help individuals and businesses accurately track transactions, calculate tax obligations, and ensure regulatory compliance. Understanding how taxes apply to your holdings is crucial, especially since tax rates vary based on how long you’ve held the cryptocurrency:

- Short-term сapital gains: If you held the cryptocurrency for less than a year, you’ll pay taxes at your ordinary income tax rate, which can range from 0% to 37% depending on your income level.

- Long-term capital gains: If you held the cryptocurrency for a year or more, you’ll pay taxes at a lower long-term capital gains tax rate. This rate can be 0%, 15%, or 20% depending on your income.

Crypto Compliance: Key Regulations and Consequences of Non-Compliance

Key Basel III Requirements for Banks and Crypto Assets

Types of crypto tax events

Selling for fiat

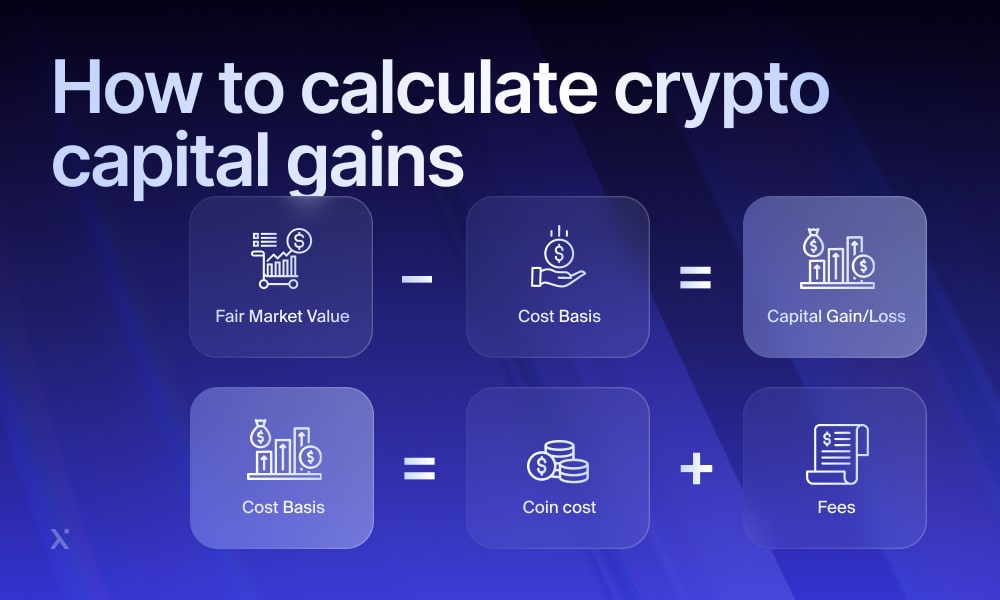

Selling your digital assets for traditional currency, like USD or EUR, triggers a taxable event. The profit or loss is calculated by subtracting your purchase price (basis) from the selling price (fair market value).

Trading for goods or services

Exchanging cryptocurrency for tangible items or services is also considered a taxable event. The value of the goods or services received is treated as the selling price for tax purposes.

Swapping for other cryptos

Trading one digital asset for another, whether on a centralized exchange or through peer-to-peer transactions, can result in taxable gains or losses. The fair market value of the cryptocurrency received is used to determine the taxable amount.

Earning crypto as income

If you receive cryptocurrency as payment for goods or services, it’s generally considered taxable income. The fair market value of the crypto at the time of receipt is the income amount.

Forking and airdrops

Hard forks and airdrops can result in the distribution of new digital assets. If you receive new tokens as a result of holding existing coins, these may be taxable depending on the specific circumstances and jurisdiction.

Mining and staking rewards

Engaging in mining or staking activities can generate cryptocurrency rewards. These rewards are generally considered taxable income when received, with the fair market value at the time of receipt being the taxable amount.

Other dispositions

Any other action that results in a change in your ownership of a digital asset can potentially trigger a tax event. This includes gifting, donating, or inheriting cryptocurrency.

Examples of сrypto tax events

Buying cryptocurrency

Imagine purchasing one Bitcoin in early 2019 for approximately $3,700. Fast forward to late February 2022, and the value of that same Bitcoin has surged to $38,500. This substantial increase in value has potential tax consequences.

If you were to use this Bitcoin to buy a car, the transaction would involve several tax considerations:

Car seller’s perspective:

The seller must report the transaction as income. However, the income is not based on the original purchase price of the Bitcoin but rather on its fair market value at the time of the transaction. This means the seller would report income of $38,500.

The seller may also realize a capital gain or loss. If they purchased the car using fiat currency (like USD) and had held the Bitcoin for more than a year, any difference between the purchase price of the Bitcoin and its fair market value at the time of sale would be considered a long-term capital gain or loss.

Buyer’s perspective:

The buyer (you) would typically report a capital gain on the Bitcoin. The gain is calculated by subtracting the original purchase price ($3,700) from the fair market value at the time of the transaction ($38,500), resulting in a gain of $34,800. This gain is generally considered a long-term capital gain if you held the Bitcoin for more than a year.

Bitcoin Ordinals 101: Your Guide to Bitcoin NFTs

All key aspects of the SEC's approach to crypto are covered in our detailed article. Read on right here

Cashing оut сryptocurrency

To calculate your tax liability, you’ll first need to determine the cost basis — the original price you paid for the coins, including any fees associated with the purchase.

Once you know your cost basis, you can compare it to the fair market value of the cryptocurrency at the time of sale. If the fair market value is higher than your cost basis, you’ve realized a capital gain. Conversely, if the fair market value is lower, you’ve incurred a capital loss.

The difference between the fair market value and the cost basis is the taxable amount if you have a gain, or the reportable amount if you have a loss.

Cryptocurrency mining

Those who engage in cryptocurrency mining effectively verify transactions on a blockchain network and are rewarded for their efforts with cryptocurrency. This compensation is generally considered an income, so you’ll need to pay taxes on crypto.

However, the specific tax treatment depends on whether the mining activity is pursued as a personal hobby or as a business enterprise. If mining is considered a hobby, the cryptocurrency earned is typically taxed as ordinary income.

Conversely, if mining is treated as a business, the income generated is reported as business income. This allows miners to deduct expenses related to their mining operations, such as the cost of mining hardware, electricity consumption, and other associated costs.

It’s important to note that the IRS closely scrutinizes cryptocurrency mining activities, and miners must accurately report their income and expenses to avoid potential tax penalties. Consulting with a tax professional can help navigate the complexities of cryptocurrency taxation and ensure compliance with tax regulations.

How to Create a Mining Pool? A Step-by-Step Guide With Real-Life Case Studies

A complete guide to crypto-asset reporting framework and DAC8 – read here

Cryptocurrency staking

If you own cryptocurrency that belongs to a blockchain that uses staking, you’ll be required to pay income tax on any rewards you receive. Staking is when you lock your cryptocurrency on the blockchain as collateral for becoming a transaction validator and being paid for it. Transactors pay fees to the validators on these blockchains, and any fees you receive are taxed as income in the year you receive them.

Because you’re paid in cryptocurrency, you must report any capital gains or losses if you use or convert the cryptocurrency. This means that if you sell your staked cryptocurrency for more than you paid for it, you’ll have to pay capital gains tax on the difference. However, if you sell it for less than you paid for it, you’ll have a capital loss.

In addition to the above, there are a few other things to keep in mind regarding cryptocurrency staking and taxes:

- The frequency of staking rewards can vary depending on the blockchain. Some blockchains pay out rewards daily, while others pay out rewards weekly or monthly.

- The amount of staking rewards you receive will depend on the amount of cryptocurrency you stake and the overall performance of the blockchain.

- Staking rewards are typically paid out in the same cryptocurrency that you staked. However, some blockchains may pay out rewards in a different cryptocurrency.

Exchanging cryptocurrencies

When you trade one crypto for another, you are essentially selling the first crypto for fiat currency and then using that fiat currency to buy the second crypto. Any profit or loss from this transaction is subject to capital gains tax.

To calculate your capital gains tax on a cryptocurrency exchange, you will need to determine the fair market value of both the cryptocurrency you sold and the cryptocurrency you purchased at the time of the transaction. The difference between the fair market value of the cryptocurrency you sold and the fair market value of the cryptocurrency you purchased is your capital gain or loss.

To cater both professional and novice traders, we tailor user-friendly and flawlessly secure cryptocurrency exchange apps, web and mobile – contact us to discuss your project

How is crypto taxed in the US? IRS rules

The Internal Revenue Service (IRS) has been increasingly vigilant about cryptocurrency transactions, defining digital assets as “any digital representations of value recorded on a cryptographically secured distributed ledger or any similar technology”.

In recent years, the IRS has made it clear that cryptocurrency transactions are subject to federal income tax. Taxpayers are now required to report any dealings with digital assets on their Form 1040, indicating whether they have engaged in such transactions. This explicit question leaves no room for ambiguity or excuses.

If a taxpayer acknowledges having dealt with digital assets, the IRS expects to see Form 8949 filed, which tracks capital gains or losses from these transactions. Failure to report taxable cryptocurrency transactions can result in significant penalties.

How to report taxes on crypto

Cryptocurrency ownership introduces unique tax considerations that require meticulous record-keeping. Unlike traditional investments, tracking cryptocurrency transactions often involves more granular detail. Every purchase, sale, or trade should be meticulously logged, capturing both the acquisition cost and the asset’s fair market value at the time of the transaction. This information is crucial for accurately calculating capital gains or losses when filing your taxes.

To streamline this process, many cryptocurrency exchanges and brokers issue 1099 forms, providing a consolidated overview of your trading activity. However, for a more comprehensive and customizable approach, consider blockchain-based tax reporting platforms. These tools can automate data collection, categorization, and analysis, ensuring you have all the necessary information at your fingertips.

When tax time arrives, cryptocurrency capital gains and losses are typically reported on IRS Form 8949, along with other capital assets. Due to the complexities and nuances of cryptocurrency taxation, consulting with a tax professional is highly recommended, especially for those new to the space.

Which Countries and Businesses Accept Bitcoin Payments?

Overview of DeFi Security Challenges and Best Practices to Overcome Them

Crypto taxes FAQ

Q: When does cryptocurrency become taxable?

A: Cryptocurrency is generally taxable when it is sold, exchanged, or used to purchase goods or services. This includes income from mining, staking, airdrops, and other forms of crypto acquisition. Additionally, cryptocurrencies received as wages or salaries are treated as ordinary income. However, holding cryptocurrency without selling or trading it is not taxable.

Q: Is the IRS able to monitor cryptocurrency transactions?

A: Yes, the IRS has become increasingly adept at tracking cryptocurrency transactions. They utilize various methods to monitor the market, including 1099 Forms, partnerships with blockchain analytics firms, and subpoenas.

Q: Do US crypto exchanges share information with the IRS?

A: Yes, all US-based cryptocurrency exchanges are required to report information to the IRS under the Bank Secrecy Act. This means that major exchanges like Coinbase, Gemini, Kraken, and Bitstamp are obligated to provide data on their customers’ transactions to the Internal Revenue Service. This information helps the IRS track crypto activity and ensure that taxpayers are reporting their gains and losses accurately.

Q: Are there consequences for not reporting crypto gains?

A: Penalties can include fines of up to 75% of the unpaid tax, interest charges on the overdue amount, and potential criminal prosecution. In some cases, those who deliberately fail to report crypto gains may face imprisonment. If you receive a warning from the IRS regarding your crypto tax reporting, it’s crucial to consult with a qualified tax professional to address the issue promptly and avoid further penalties.

Q: How do I find the basis of cryptocurrency I bought with real money?

A: Your basis, also known as your cost basis, is the amount you paid to acquire the cryptocurrency, including fees, commissions, and other acquisition costs in U.S. dollars. Your adjusted basis is your basis adjusted for certain expenditures, deductions, or credits.

Q: What are the tax implications of exchanging crypto for other assets?

A: Exchanging virtual currency for other property, including goods or different cryptocurrencies, can trigger capital gains or losses. The gain or loss is calculated by comparing the FMV of the received property to the basis of the virtual currency exchanged.

Q: What are the tax implications of a hard fork without receiving new cryptocurrency?

A: A hard fork creates a new cryptocurrency on a separate blockchain. If you hold the original cryptocurrency and don’t receive any of the new cryptocurrency (either through an airdrop or other transfer), you generally won’t have taxable income.

Q: How do I determine the FMV of cryptocurrency received on a trading platform?

A: For cryptocurrency received through a centralized or decentralized exchange, the FMV is typically the U.S. dollar value recorded by the exchange for the transaction. If the transaction is off-chain, the FMV is the price the cryptocurrency was trading for on the exchange at the time the transaction would have been recorded on-chain.

Summing up

The cryptocurrency market, while offering immense potential, also presents unique challenges when it comes to taxation. The evolving nature of digital assets and the intricacies of US tax laws can make it difficult for investors to accurately report their crypto-related income.

If you’re considering starting a cryptocurrency pool or exchange, it’s essential to fully grasp the tax implications and legal regulations that apply to these ventures. In such matters the importance of consulting a qualified custom blockchain solutions company cannot be overstated. Our experts can provide invaluable guidance on:

- Understanding tax implications: We can help you identify which crypto activities are taxable and which are not, ensuring compliance with IRS regulations.

- Accurate reporting: We can assist in tracking your crypto transactions and calculating the appropriate tax liabilities.

- Avoiding penalties: By working with our team, you can minimize the risk of penalties and fines associated with non-compliance.

By partnering with a reputable blockchain consulting company like PixelPlex, you can gain the expertise and support needed to effectively manage your crypto assets and ensure compliance with US tax laws.

Let’s partner to turn your crypto holdings into substantial returns. Get in touch with our team here.