Have you ever stopped to think about how quickly the world of finance is changing? Cryptocurrencies are now a mainstream phenomenon. But here comes a question: how do we keep track of it all, especially for tax purposes?

The world of cryptocurrency is exciting, but navigating the tax implications can feel like deciphering ancient hieroglyphics. A 2023 study by Statista found over 300 million global crypto users, highlighting the potential tax revenue at stake.

If you’re a business operating in the crypto-asset space (e.g., managing crypto exchanges, crypto banking solutions, decentralized wallets), understanding regulations like the Directive on Administrative Cooperation in the field of taxation (DAC8) and the OECD’s Crypto-Asset Reporting Framework (CARF) is extremely important. They impact how you report your crypto holdings and transactions, potentially saving you headaches (and tax dollars) down the line.

The frameworks specifically target information exchange between countries to combat tax evasion, money laundering, and other illicit activities that can thrive in anonymous transactions.

In this comprehensive guide, we’ll break down DAC8 and CARF in simple terms, explaining their key features, how they work together, and most importantly, what they mean for your business.

Are Corporate Crypto Stashes The Future? A No-Nonsense Guide to DATs

Key Basel III Requirements for Banks and Crypto Assets

An introduction to the crypto-asset reporting framework

CARF is a new set of rules for countries to share information about cryptocurrency transactions. Think of CARF as a bridge between the innovative world of crypto and the established world of taxation. Its goal is simple: to ensure everyone plays by the same rules. This framework aims to make things smoother for both taxpayers and governments.

Why is the crypto-asset reporting framework so important? Well, imagine a world where crypto transactions happen under the radar. It would be a nightmare for tax collection, and frankly, not very fair. Crypto compliance solutions, including CARF, help prevent tax evasion, promote transparency, and ensure everyone contributes their fair share. They also provide valuable data for governments to better understand this rapidly growing market.

How does CARF work?

In a nutshell, it establishes a standardized system for collecting and exchanging information on crypto-asset transactions. This means that crypto exchanges and other service providers will be required to report certain details about their users’ activities to tax authorities.

Here’s the breakdown of CARF’s key features:

- Scope: Crypto-asset reporting framework focuses on crypto-assets (fungible, security, utility tokens, NFTs, native cryptocurrencies) that function similarly to traditional securities, meaning they can be traded and potentially generate a profit.

- Who’s involved? Crypto service providers like exchanges, custodians, and wallet providers are the ones responsible for collecting and reporting user data.

- Transaction transparency: CARF aims to capture details on a variety of crypto transactions, including purchases, sales, transfers, and even income earned through staking or lending crypto assets.

- Due diligence: It includes guidelines for crypto service providers to verify your identity and determine your tax residency. This helps ensure the information being reported is accurate.

Why is CARF important?

The rollout is still in its early stages (with some countries targeting implementation by 2027), but the impact is likely to be significant in the coming years. Here are some potential outcomes:

- Fairness for everyone: By ensuring everyone pays their fair share of taxes on crypto gains, crypto-asset reporting framework helps maintain a healthy and competitive financial system.

- Combating crime: Cryptocurrency’s anonymity has unfortunately attracted some bad actors. CARF can be a powerful tool for identifying and stopping illegal activities like money laundering and tax evasion.

- Building trust: Transparency breeds trust, and trust is essential for the long-term growth and stability of the crypto market. CARF helps to legitimize cryptocurrencies and attract more mainstream investors.

- Increased tax revenue: Governments are likely to see a boost in tax revenue as crypto gains are properly reported and taxed.

- Market maturation: With greater transparency, the crypto market could become more mature and attractive to institutional investors.

CARF allows authorities to track suspicious transactions that could be linked to criminal activity. Here’s our list of key cybersecurity threats businesses should be aware of in 2024

Of course, there are also questions and concerns surrounding CARF. Privacy is a major one, and it’s important to ensure that data is collected and shared securely. Additionally, the specific implementation of the crypto-asset reporting framework might vary from country to country, so staying informed about local regulations is key.

Enterprise Blockchain: Prom Promise to Profit

DAML Development Services: Everything You Need to Know

Canton.Network Explained: How It Solves DeFi's Biggest Risks

The scope of the OECD crypto-asset reporting framework

The rapid rise of cryptocurrencies has governments scrambling to ensure tax compliance. A key tool in this effort is the OECD’s Crypto-Asset Reporting Framework, but what exactly does it cover?

A look at different cases of crypto-assets

Here’s a breakdown of some key categories:

Payment tokens. Designed primarily for making transactions, these include Bitcoin, Ethereum, and Litecoin.

Security tokens. These represent ownership in a real-world asset, like real estate, shares of a company, or investment funds. It estimates that security tokens could reach a market size of $10 trillion by 2025, underlining the need for clear tax regulations.

Utility tokens. Grant access to a specific service or platform. While their value may fluctuate, they don’t necessarily represent an investment. The line between utility tokens and securities can be blurry, making OECD CARF’s guidance crucial for proper classification.

If a utility token is used for its intended purpose (e.g., accessing a game), the transaction might not be taxable under OECD CARF. However, if the token is bought, held, and then sold for profit, it could be considered a taxable event.

Carving out exceptions: are NFTs in or out?

OECD CARF focuses on capturing tax information from transactions involving fungible crypto-assets – those where one unit is identical to another. This raises questions about NFTs and specific types of utility tokens.

NFTs represent unique digital assets, like artwork or collectibles. Due to their one-of-a-kind nature, NFTs may fall outside the scope of CARF’s current reporting requirements. However, sales of high-value NFTs could still attract tax scrutiny.

NFT Launchpad Development: A Comprehensive Guide Based on PixelPlex’s Expertise

Non-Fungible Tokens (NFTs): A Booming Trend From the Blockchain World

Take a look at the top 10 blockchain platforms preferred by popular projects for launching their NFTs

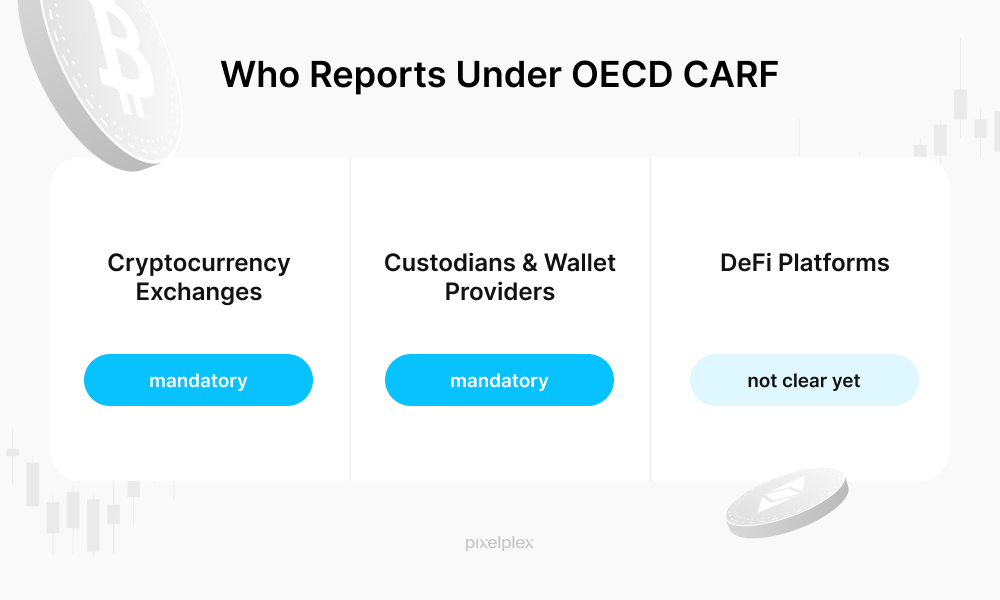

Who will have to report?

The following organizations are subject to OECD CARF requirements:

Cryptocurrency exchanges. They’ll be responsible for collecting user data and transaction details, ensuring everything from your identity to your latest swap is reported to the tax authorities.

Custodians and wallet providers. They’ll likely be required to report your holdings and activity to the relevant tax authorities.

DeFi platforms and the grey area. Unlike centralized exchanges, DeFi platforms operate on a peer-to-peer basis, often without a central authority. This raises questions about who is responsible for reporting under the crypto-asset reporting framework.

The anonymous nature of some DeFi transactions makes it difficult for authorities to track and identify participants. As DeFi continues to evolve, regulators are likely to develop new frameworks to address the reporting challenges it poses.

What transactions get reported under OECD CARF?

CARF aims to bring clarity, outlining activities that trigger reporting requirements.

Below our cryptocurrency exchange development company shortlisted the key transactions that fall under CARF.

Traditional trades

Buying or selling cryptocurrencies on exchanges like Bitcoin or Ethereum will trigger an OECD CARF report. This includes both spot trades (immediate exchanges) and futures contracts (agreements to buy or sell at a predetermined price in the future). Grand View Research shows that by 2030, the cryptocurrency market is expected to grow by 12,5%, highlighting the vast scope of transactions CARF aims to monitor.

Peer-to-Peer (P2P) transactions

Swapping crypto directly with another individual can also be captured by CARF, depending on the platform facilitating the exchange. Many P2P platforms now integrate with CARF-compliant systems to ensure reporting.

Step-by Step Guide to P2P Crypto Exchange Development

How to Develop a Peer-to-Peer Lending Application: PixelPlex’s Detailed Guide

Transfers

Moving crypto between your own wallets, even if across different exchanges, generally won’t trigger an OECD CARF report. However, transfers to third-party wallets might be reported, particularly for large sums.

Staking

The process of locking up crypto holdings to validate transactions on a blockchain network can earn rewards. These staking rewards are considered income under CARF and may be subject to reporting.

Lending

Providing your crypto holdings to a lending platform to earn interest falls under OECD CARF. The interest earned on these loans is considered taxable income.

Airdrops & forks

Receiving free crypto through airdrops or hard forks may be considered income depending on the jurisdiction and could be reportable under the crypto-asset reporting framework.

An introduction to the DAC8 proposal

The OECD is not alone in its efforts to bring greater transparency to the crypto-asset space. The EU has also developed a framework with similar objectives – DAC8.

The Directive amending the EU rules states:

“The provisions of DAC8 on due diligence procedures, reporting requirements, and other rules applicable to crypto-asset service providers largely reflect the Crypto-Asset Reporting Framework (CARF) and a set of amendments to the Common Reporting Standard (CRS), which were prepared by the OECD under the mandate of the G20.”

This alignment between DAC8 and the crypto-asset reporting framework signifies a coordinated global approach towards regulating the crypto-asset market. If countries use the same rules, it would create a fairer environment for all and strengthen global efforts to fight financial crime.

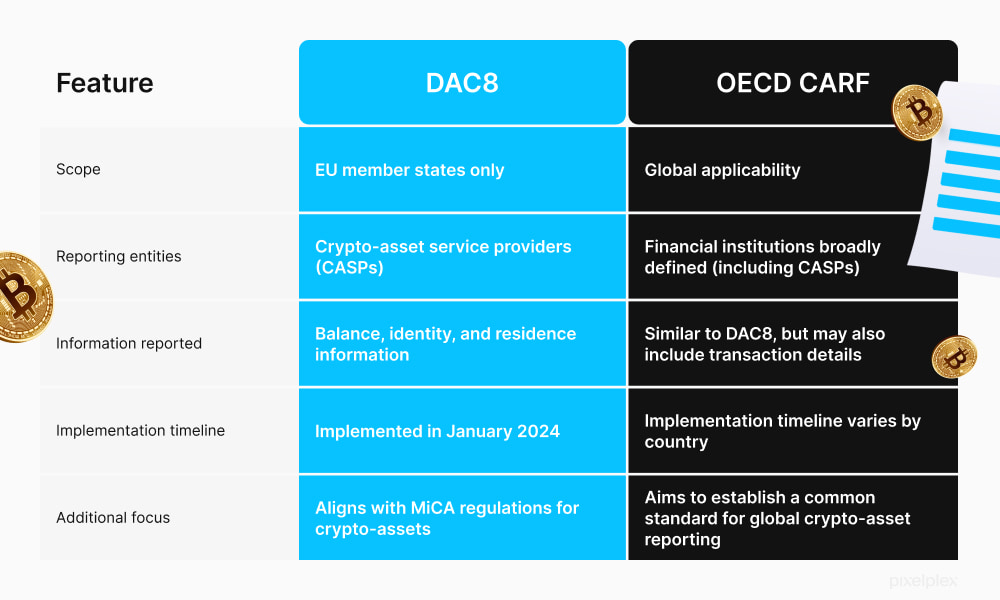

DAC8 vs CARF

While both the EU’s DAC8 and the OECD’s CARF share the same core goals of bringing transparency and accountability to crypto transactions, their implementation details differ slightly. The infographic describes these key distinctions, highlighting the nuances between the two frameworks.

The key DAC8 reporting requirements

Here’s the breakdown of DAC8’s key features:

- Who’s on the hook? Crypto exchanges, custodians, and wallet providers.

- What needs to be reported?

- Identity: User details like name, address, and tax identification number.

- Account information: Account numbers, types of crypto-assets held, and balances.

- Transaction details: Dates, types, and values of crypto purchases, sales, transfers, and even income earned through staking or lending crypto assets.

- KYC procedures. To ensure the accuracy of reported data, DAC8 emphasizes robust KYC procedures. CASPs will need to verify user identities and determine their tax residency status.

- Deadlines. EU member states are required to implement DAC8 into their national laws by December 31, 2025, and crypto asset service providers must comply with its reporting obligations starting January 1, 2026.

Take a look at our digital solution that helps maintain control over your operations, detect fraud and remain compliant

Summing up

While the EU’s DAC8 and the OECD’s CARF have distinct names and may have originated from different governing bodies, both frameworks achieve the same core objective: fostering transparency and accountability in crypto transactions.

They establish a standardized approach for collecting and reporting crypto-asset data, ensuring that tax authorities have a clear view of this growing financial landscape. While there might be slight variations in implementation details, both DAC8 and CARF ultimately work in tandem to bring the world of cryptocurrencies under a more regulated umbrella.

If you’re looking to navigate the ever-evolving crypto landscape with confidence, consider partnering with PixelPlex’s blockchain consulting and blockchain product development team.

Our team possesses the knowledge and experience to guide you through every step of your journey, from comprehensive smart contract audits and STO development services to DeFi solution implementation and p2p crypto exchange development, ensuring your projects are built on a secure and future-proof foundation.

Moreover, we have developed our own proprietary solution, OTC Hawk. This wealth and portfolio management app provides users with the ability to explore a wide range of cryptocurrency trading strategies, uncover new opportunities, track signals, and much more.

Let’s connect and discuss how we can empower your crypto journey. Reach out to us today and let’s create innovative solutions tailored to your needs.