Having been on the market for a while already, blockchain proved to be a disruptive technology that could benefit multiple industries. Yet, despite being a hot topic, some people are still not sure what blockchain is.

Whether you are a crypto enthusiast or a regular user, you have probably heard about blockchain. The open-source technology has gone far beyond crypto projects finding its application in many industries, from banking and finance to healthcare and real estate.

In addition, blockchain has become the basis for multiple ground-breaking concepts, including NFT development, metaverse projects, and Web3 initiatives.

Overall, it is estimated that by 2024, the global blockchain technology market will generate $20 billion. In 2021 alone, the world has spent $6.6 billion on blockchain solutions.

But what exactly is blockchain and what are its common use cases? Read our Blockchain Explained article to find a detailed explanation of this technology accompanied by blockchain pros and cons, top blockchain platforms, and key blockchain use cases across industries.

What is Blockchain?

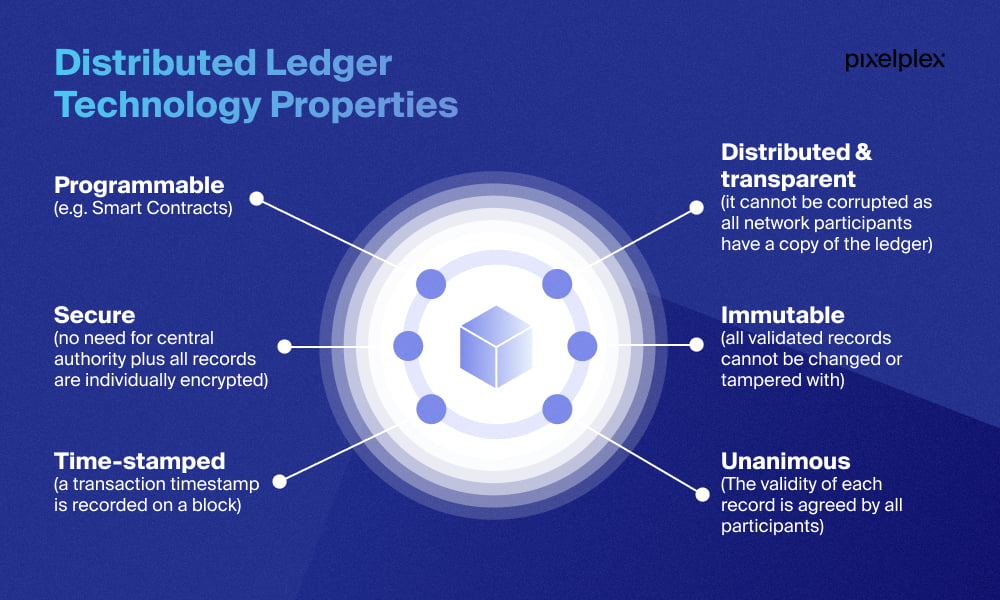

Blockchain is a decentralized network that records information in a way that makes it difficult or nearly impossible to change, hack, or tamper with. Basically, blockchain technology is a digital ledger of transactions that is distributed across a network of computer systems.

How does blockchain work? The blockchain ledger explained

Blockchain consists of multiple blocks that, forming a linear set, record transactions. Each block holds a set of information. When block storage capacity is filled, it is closed and linked to the previously filled block, thus forming a chain of data known as blockchain.

The blocks are distributed across all users of the blockchain network, so every user has a copy. None of the users hold administrator rights over the network, which makes the blockchain network decentralized. The decentralized database managed by multiple users is known as distributed ledger technology.

Blockchain was first introduced by Satoshi Nakamoto in 2008 as part of the bitcoin cryptocurrency. Bitcoin blockchain prevented central authority from issuing currency, managing ownership and financial transactions. This was the first application of blockchain technology and it has laid the platform for future development of the new concept of decentralization in other industries besides financial.

These days, blockchain technology is seen as an approach to software architecture development that involves creating a decentralized network of interconnected users (nodes) where certain “consensus mechanisms” are applied in order to store, manage and modify information they hold, while all interactions (transactions) are secured by the process of cryptography.

Let’s dive a bit deeper into this groundbreaking technology to make sure we have blockchain explained fully, leaving no gray areas.

Blockchain technology explained: what are the four components of blockchain?

Blockchain architecture consists of the four key components, including:

# 1 Blockchain network

# 2 Consensus mechanism

#3 Smart contracts

#4 Permissions

Let’s deep dive into each of the blockchain components.

Blockchain network

The blockchain network is a data structure which stores data and information on manipulation of this data within a semi-public chain of linear containers (blocks). Any user of the blockchain can see and verify that information has been placed in a block because these blocks have the signature of its owner on it. Only the owner holds private keys (hash data) and has the right to access data stored within the block.

An important trait of a blockchain network is its immutability: this means that once a transaction has been recorded, it can never be erased from the system. The blockchain behaves similar to a database with the exception that part of its information (the header) is public. Thus the main principles of blockchain are public visibility and private inspection.

Let’s try to have this concept of blockchain explained using simple words. Think of it as a home address. The address can be made public and posted in an address database, however, only the owner of the house has a private key and is able to enter. Another important point here: once the owner has claimed that address as their own, nobody else can claim this address.

Consensus mechanism

Blockchain consensus mechanisms also known as consensus algorithms are fault-tolerant mechanisms that are used to achieve an agreement on a single state of the network in real time. A goal of a consensus mechanism is to ensure that there exists only one valid copy of a record shared by all the nodes.

In contrast to centralized models, a decentralized consensus establishes trust through a decentralized network of nodes. The nodes constantly record transactions into public “blocks”, creating the “blockchain”. Each block contains hash data of the previous action (transaction).

But before a transaction is added to the blockchain, it must be authorized and this is when we have to make blockchain validation explained. Blockchain uses cryptography to authenticate the transaction source, eliminating the need for a central authority to validate the transaction. The nodes enter into an agreement (consensus) on whether the transaction was valid and that the block is worthy to be added to the blockchain.

There are different types of consensus mechanisms that are aimed at achieving agreement, trust, and security across a decentralized computer network.

What are the most popular consensus mechanisms?

At the heart of first-generation blockchain networks stood the “proof-of-work” mechanism, which is key to Satoshi Nakamoto’s original vision and role of blockchain as the explicit authenticator of transactions.

The Proof of Work (PoW) consensus model is the mechanism used to maintain participation in block creation on the blockchain network. It is manifested as a “hard enough task” that is imposed on users to prevent them from making illegal changes to records in the blockchain. The proof of work is secured via the strength of cryptographic hashes that ensure its authenticity.

The blockchain platforms that leverage PoW consensus mechanisms benefit from a high level of decentralization and increased security. Yet, PoW has significant limitations, including slow speed of transactions and significant energy consumption.

If we take, for example, Bitcoin, which relies on the Proof of Work consensus mechanism, the electricity demand for it increased from 7 TWh in April 2017 to 151.2 TWh in April 2022, which is a 20-fold increase in only 5 years.

Another prominent platform that currently relies on the PoW consensus is Ethereum. According to Digiconomist, Ethereum consumes 69.76 TWh, which can be compared to the power consumption of Check Republic.

These limitations have made the Proof of Work concept actively being replaced by the Proof of Stake (PoS) blockchain consensus model. In it, transactions are secured by users of the blockchain network who play the role of validators. To validate transactions, validators must hold a certain percentage of the network’s total value.

This concept leads to reduced usage of system and hardware resources. Proof of stake might also provide increased protection from malicious attacks on the network by making it very expensive to execute attacks, and, therefore, reducing the incentive for those attacks.

As for the examples of currently leading PoS-based blockchains, these include: Polkadot, Cardano, and Avalanche. Moreover, Ethereum is currently in the process of moving to Ethereum 2.0 – a PoS-based blockchain.

Don’t miss ourEthereum vs Polkadot comparison article to find out the pros and cons of both platforms

Other prominent consensus mechanisms include:

- Delegated Proof Of Stake (DPoS). DPoS is a high-speed consensus model, most known for its first implementation in EOS blockchain. Delegated Proof of Stake mechanism is a type of consensus where users can stake their coins to participate in voting for a number of delegates. The weight of a user’s vote depends on the stake. Delegates that have received the highest amount of votes are allowed to take part in block creation and get rewarded for creating these blocks.

- Proof of History (PoH). In contrast to other consensus mechanisms, where the nodes rely on external sources of information when assigning a “median” timestamp during transaction validation, PoH offers an internal clock mechanism. The mechanism always displays the same time for all the nodes in the network/.

- Proof of Authority (PoA). A mechanism where instead of staking coins, validators are staking their identity. Suits best private blockchain networks.

- Proof Of Capacity (PoC). PoC is a model where consensus is achieved via a process called plotting. Instead of using computational power to create solutions, they are pre-stored in digital storages. The owner of the fastest solution to the puzzle gets to create the new block. Users who have the most storage capacity on the blockchain have the highest odds of creating a new block.

There are also blockchains with pluggable consensus, which means they can incorporate various consensus mechanisms depending on the business goals that need to be achieved.

Permissions in Blockchain

Blockchains can be permissioned or permissionless. Permissionless blockchains are open networks allowing everyone to participate in the consensus process that a blockchain applies to validate transactions.

A permissioned blockchain introduces digital certificates which act as a regulation of access to transaction details. This enables the use of policies to constrain network usage.

Applying these constraints to the blockchain network allows organizations to easily comply with data governance regulations, such as the Health Insurance Portability and Accountability Act (HIPAA) or General Data Protection Regulation (GDPR). Permissioned blockchains are also much more effective in maintaining the consistency of data appended to the network.

Smart contracts

Smart contracts are the building blocks for decentralized applications or DApps. Smart contract development services help implement a little program or written code that you can entrust with a unit of value.

The basic idea behind smart contracts is that a transaction’s contractual governance between two or more parties can be verified programmatically via the blockchain, instead of via a central arbitrator, rule maker, or other intermediaries. Users of this technology can formulate the terms and implications of their agreement programmatically and conditionally, with automatic money releases when services are provided or inflict penalties if the terms are not met.

Blockchain explained: who are network participants in blockchain?

A well-functioning blockchain generally includes the following network participants:

- Users: typically a business user with permissions to join the blockchain network and execute transactions with other network users;

- Regulator: A blockchain user with permissions to oversee transactions executed within the blockchain network. Regulators may be prohibited from making their own transactions;

- Blockchain developer: Programmers who create the apps and develop smart contracts to enable blockchain users execute transactions and exchange various information on the blockchain network. Apps serve as an interface between users and the blockchain;

- Blockchain network operator: users who have special permissions and authority to define, create, manage and monitor the blockchain network. Each business on a blockchain network has a blockchain network operator;

- Certificate authority: a user who issues and manages different types of certificates required to run a permissioned blockchain. Certificates can be issued to blockchain users or to individual transactions.

Blockchain layers explained: what are Layer 1 and Layer 2?

Layer 1 refers to the blockchain network itself while Layer 2 protocol is a third-party integration used in conjunction with the Layer 1 blockchain network to solve its inefficiencies such as poor scalability and slow transaction speeds.

To help you understand the necessity of Layer 2 solutions, we need to have a blockchain trilemma explained. It is a belief that blockchains can only provide two of the three benefits at any given time. These benefits include decentralization, security, and scalability.

If we take Ethereum as an example, the blockchain provides for increased security and high levels of decentralization. At the same time, one of the core Ethereum’s problems is scalability. The current Ethereum network supports only about 30 transactions per second (TPS).

That is why Ethereum needs Layer 2 solutions – protocols built on top of the existing blockchain network with the goal to tackle its inefficiencies. One of such examples is Arbitrum – Ethereum’s Layer 2 scaling solution which provides for 40,000 TPS.

Aptos Blockchain: a Detailed Guide

Want to gain more insights on Layer 2 solutions? Check out our detailed guide

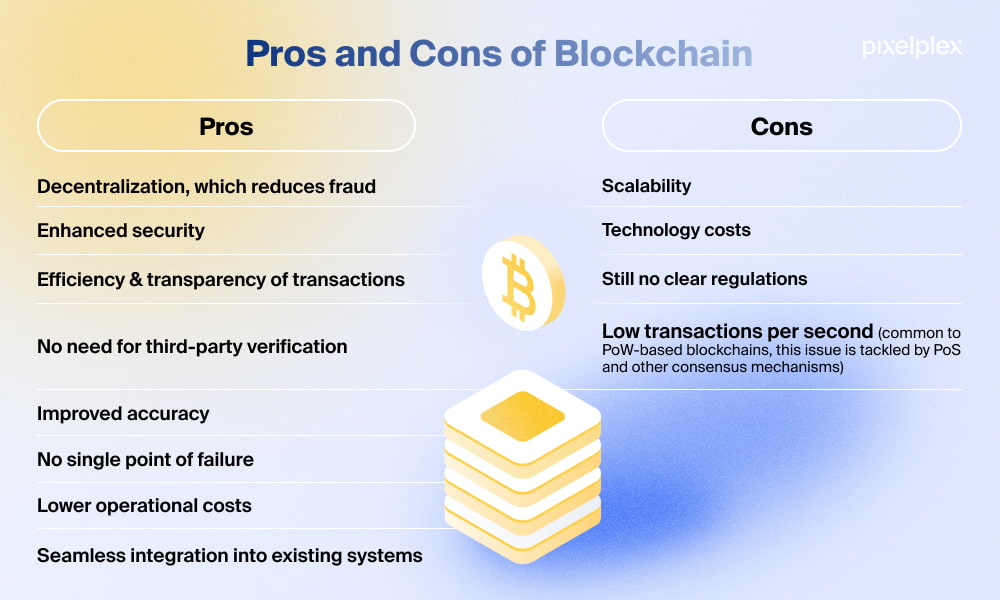

Blockchain explained: what are the pros and cons of blockchain?

Some of the most prominent benefits of blockchain technology include decentralization, which means that there is no need for a third party to make a transaction, security as it is tough to tamper with records once they are in blockchain (digital copies are checked against each other automatically), and low operational costs associated with no payment processing or banking fees.

As for the major cons of blockchain, these include poor scalability meaning that blockchain can handle fewer transactions per second (yet, there are solutions like Layer 2 protocols that solve these issues) and high technology costs as blockchain requires enormous amounts of energy.

Take a look at the infographic below to quickly compare all the major pros and cons of blockchain.

Now that we have the core components, layers, user types, and pros and cons of blockchain explained, let’s take a look at the different types of blockchain networks (platforms) that have emerged on the market after the first implementation of a blockchain, Bitcoin.

Blockchain explained: what are the top blockchain platforms?

At present, the most prominent and established blockchains on the market include Ethereum, Hyperledger Fabric, Ripple, Stellar, EOS, R3 Corda, Tezos, IBM Blockchain, Quorum, and Echo. These are the platforms that provide the right software development environment to allow the creation of decentralized apps (dApps) which can be stored and executed on multiple nodes of the blockchain network. Our blockchain consulting experts prepared a detailed description of each platform.

Ethereum

The first blockchain platform to be introduced back in 2015 was Ethereum. It is a distributed computing platform with PoW consensus and its own Ethereum Virtual Machine, which provides a run-time environment for smart contract and dApp development and handles transactions and computations on the blockchain.

Ethereum is by far one of the most popular blockchain platforms. At present, there are nearly 3K dApps on top of the Ethereum platform. Yet, due to its limitations like poor scalability and high transaction costs, it contributed to the creation of numerous other blockchain platforms aiming to solve Ethereum’s issues.

Hyperledger Fabric

Hyperledger Fabric is an open-source, permissioned blockchain development framework with modular architecture, pluggable consensus and membership services. It leverages container technology called “chaincode”, enabling it to host smart contracts and allowing it to be configured and deployed to various environments. It is an enterprise-grade solution used across a broad set of industries.

EOS

EOS is an open-source, cross-industry, permissioned blockchain. It was the first to introduce the DPoS consensus model, which, in combination with multi-threading architecture, allows for decentralized application’s hosting, decentralized storage of enterprise solutions and smart contract capability, solving the scalability issues of Ethereum and Bitcoin blockchains. It supports thousands of commercial scale dApps and provides inter-blockchain communication.

Ripple

Ripple is an open-source, financial industry-focused, permissioned blockchain platform with a probabilistic voting consensus mechanism in place. Although it does not provide smart contract capability, it is designed to connect banks, payment providers, digital asset exchanges and other players of the financial market through its own global payments network, RippleNet. The network has extremely low fees on global transactions and does not allow chargebacks.

Stellar

Stellar is another financial services-oriented blockchain platform. Similar to Ripple, it may be used for exchanges between cryptocurrencies and fiat-based currencies. Yet, Stellar offers smart contract functionality, which makes it possible to use it for building banking apps, smart devices and mobile wallets.

The platform has its own Stellar Consensus Protocol (SCP), a federated byzantine agreement protocol, using sequential voting and node nomination to create and approve new blocks. Having a set of provable safety properties, SCP optimizes the process of reaching an agreement by halting the progress of the blockchain network until a consensus can be reached in case of misbehaving nodes or partitions.

R3 Corda

R3 Corda is an open-source, permissioned blockchain platform with pluggable consensus model. Although it was initially designed to be used in finance, R3 Corda is now being applied in various other use cases, including healthcare, trade, supply chain management, and eGovernance. Smart contract functionality makes Corda platform applicable for development of state-of-the-art commercial, enterprise-grade DApps for any business problem, challenge or opportunity.

Quorum

Quorum is one of the first open-source enterprise-ready distributed ledger and smart contract platforms put out by such a large and well-established financial institution as JP Morgan Chase. Having a modified Ethereum core, Quorum was designed to develop and evolve alongside Ethereum. Quorum is a permissioned network with a raft-based and Istanbul BFT consensus model, which enables faster transaction speeds and higher throughput relative to permissionless blockchains.

IBM Blockchain

IBM blockchain is a platform offering a full-stack blockchain-as-a-service solution that enables users to combine their blockchain components in any way they want. The platform is built on top of the open-source Hyperledger Fabric platform. It has an intuitive interface and can be used by users who want to develop their own blockchain network.

Tezos

Tezos is an open-source decentralized blockchain that provides for executing peer-to-peer transfers and deploying smart contracts. The platform is focused on digital assets management and was built with mechanisms that ensure community governance and participation, which are the key components of Web 3.0. Tezos leverages the PoS consensus algorithm and uses the on-chain upgrade mechanism, which allows the platform to be easily adjustable and adaptable.

Echo

Echo is a product built by PixelPlex. It is a completely decentralized blockchain platform with high throughput and an advanced smart contract development ecosystem. The platform embraces a DPoS-inspired consensus mechanism to enable blazing-fast consensus, and the powerful ECHO IA-64 Virtual Machine with the richest, the most well-developed ecosystem of programming tools.

The platform was designed as an advanced smart contracts platform. Echo’s mission is to enable a wide range of blockchain developers to cooperate and take advantage of a highly scalable and efficient smart contract protocol, thus enabling a wide variety of business entities and individuals for the first time to actively and profitably participate in the blockchain revolution.

Meet Qtum – an open-source hybrid blockchain platform developed by PixelPlex blockchain developers

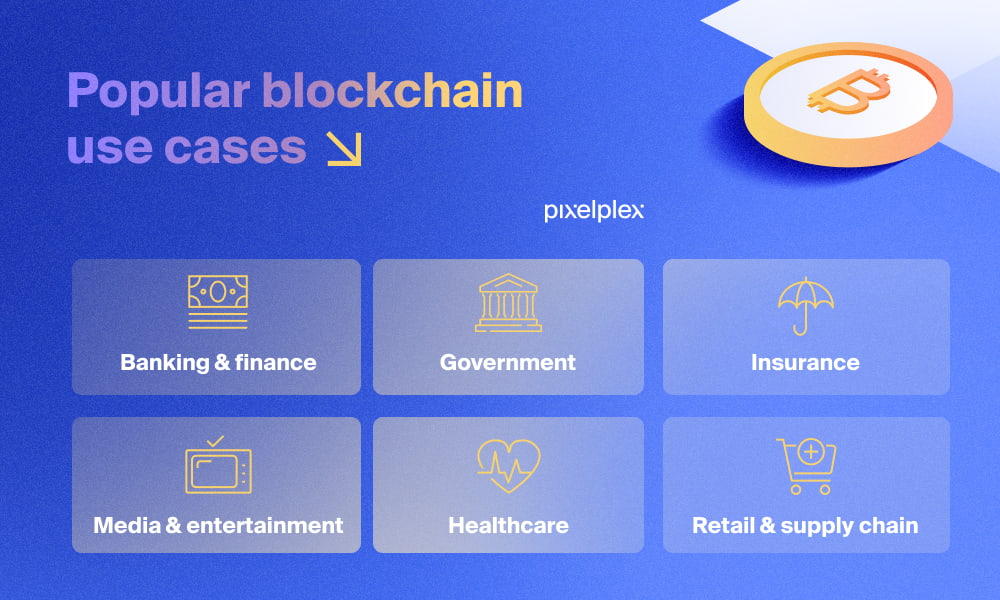

Blockchain explained: in what industries is blockchain currently used?

By providing increased security and transparency and eliminating intermediaries, blockchain technology has found itself in a wide range of industries. At present, the main blockchain use cases include such industries as banking and finance, government, insurance, media and entertainment, healthcare, and retail and supply chain. Let’s take a closer look at each of them.

Banking & finance

Blockchain technology gave birth to the concepts of decentralized banking and decentralized finance (DeFi). According to the DAppRadar report, DeFi transaction volume has grown from $21 billion in 2019 to nearly $270 billion in 2020.

Some of the most notable implementations of DeFi in banking and finance include decentralized lending and borrowing (yearn.finance, Aave), decentralized exchanges (Uniswap, Ox), and decentralized autonomous organizations (Compound, Maker).

Healthcare

Electronic medical records on the blockchain is the number one use case for blockchain in healthcare. Distributed Ledger Technology allows for a tamper-proof record of the patient’s medical history. This includes vaccines, lab results, treatment strategies and prescription history all placed in a single linear ledger stored on a decentralized network.

With permissioned blockchain networks, users can also share their personal medical information securely and safely. Also, improved medication adherence to industry standards could be achieved by storing information on the blockchain.

Some of the interesting blockchain-based healthcare projects include MedRec – a medical records management solution, and Patientory – a mobile app for managing health data.

Retail

Popular eCommerce platforms like Amazon and eBay will have to make way, adjust, or enter into partnership with emerging blockchain solution providers that solve the many issues currently troubling retailers. This includes major eCommerce platforms’ aggressive advertising of their own products, as well as presale fees causing retailers to increase prices to obtain the desired revenue amount. Strict policies hindering communication between the buyer and the seller also come into play.

Emerging blockchain network-powered marketplaces stand to solve all these problems and provide both retailers and buyers with a convenient environment and ecosystem of fair trade.

Supply Chain Management

Many companies struggle to keep track of their inventory, storage, and logistics. This leads to poor data analytics and additional expenses.

DLT/Blockchain solutions are an ideal environment to manage storage units across multiple locations and share that data with all the parties involved. Blockchain in supply chains allows for real-time tracking and viewing accurate, tamper-proof data automatically tracked by GPS and IoT devices. This creates an opportunity for more efficient routing of shipments backed by the secure storage of data on a blockchain network. DLT solutions are much more efficient at managing every aspect of shipping logistics.

Government & eGovernance

Blockchain in government can contribute to the creation of full-scale eGovernance ecosystems by providing verified IDs registered on the network. Such systems could help citizens vote, pay taxes and perform other government-related transactions with increased privacy and security.

All government transactions could be moved to the network, creating virtual residency accounts to establish identity and providing access to educational, banking, mobile communication and other services.

Blockchain-based identity gives citizens control of their personal information and allows them to decide who can access their data, eliminating the need for regulations to govern these processes.

Insurance

Blockchain also has all the necessary capabilities to change the way insurance companies function. With blockchain’s smart contracts and dApps, insurance workflows can be conducted over blockchain accounts, which contribute to more automation and tamper-proof audit trails.

Some of the most prominent use cases of blockchain in insurance include claims handling, reinsurance practices, registries of high-value items, as well as know-your-customer (KYC) and anti-money laundering (AML) procedures.

Media & entertainment

Being able to track the lifecycle of any asset, blockchain can help protect digital content and intellectual property, thus reducing piracy and fraud. It is reported that 90% of European and US entertainment companies are exploring their blockchain options.

Also, the appearance of non-fungible tokens (NFTs) – digital assets that link ownership to unique items, such as works of art, music, and videos – significantly contributes to the adoption of blockchain in the industry. Check out our recent article on NFT projects and use cases to find out what are non-fungible tokens and how they can be used across industries.

Getting back to the use of NFTs in the entertainment industry, already we can see that AMC Entertainment Holdings announced that they will accept Ether, Bitcoin, and Litecoin for ticket and concession purchases. Meanwhile, we will soon see a new science fiction movie known as Zero Contract as the first film auctioned off as an NFT.

Blockchain in Agriculture: Benefits, Use Cases and Platforms That Are Disrupting the Industry

Find out the most prominent blockchain use cases worth exploring in 2022

Closing thoughts

Blockchain is a groundbreaking technology that was first utilized to streamline financial transactions and eliminate intermediaries. However, today’s application of modern distributed ledger solutions serve a wide variety of industries such as eCommerce, supply chain management, retail, and many others.

Now that we have blockchain technology explained you know all of its potential for cross-industry application. And if you are planning to implement blockchain in your business domain, our blockchain development company and consultants will be glad to assist you with the entire development process. With 15+ years of experience and 450+ successful client stories, we can help you turn your idea into a real-life project.

Moreover, we offer our own blockchain API solution that connects dApps to blockchain networks in a flash, with zero commission, making the integration process even faster and more efficient.

Ready to see how blockchain can benefit your business? Get in touch with us to explore how we can help with your blockchain project.