AI technology has become a critical disruptor in almost every industry, and banking is no exception. Here’s everything that AI holds in store for the future of the industry.

Artificial intelligence (AI) is a constellation of multiple distinct technologies such as machine learning, natural language processing, computer vision development, and conversational interfaces. Its growing adoption in the healthcare, education, manufacturing, retail, and automotive sectors reflects how effective its algorithms, frameworks, and techniques are in dealing with complex business problems.

At the same time, the deployment of AI in finance has made the sector more customer-centric and technologically relevant. Experts point out that the banking sector must adopt AI technology if it is to remain relevant to tech-savvy customers and withstand the fierce competition posed by the FinTech players.

Read on to find out how AI technology promises to revolutionize the functioning of the banking sector and take it to new heights.

What the AI industry looks like today

We can briefly describe AI as a technology that enables machines to sense, act, comprehend, and learn with human-like levels of intelligence. AI is an extension of human capabilities and not a replacement. When complemented with the right strategies and data, AI technologies can transform any business for the better.

According to a study conducted by Gartner in 2019, approximately 37% of companies globally had already adopted AI in some form or the other. A forecast by marketsandmarkets suggests that the global AI market will grow from $58.3 billion in 2021 to $309.6 billion by 2026, exhibiting a Compound Annual Growth Rate (CAGR) of 39.7% during the forecast period. According to Grand View Research, the revenue generated from AI will grow from $93.53 billion in 2021 to $997.77 billion in 2028.

Given the benefits of AI, such as reduced operational costs and increased value to customers, financial service institutions have turned to AI technologies including chatbot assistants and fraud detection systems. According to a report by Business Insider, close to 80% of banks are aware of the potential benefits that AI presents to their sector.

Inevitably, AI represents the future. Let’s understand why.

How can AI transform banking?

Throughout the past decade of technological disruption, banks have extended the scope of their services by involving IT, retail, and telecom partners, and providing services like e-banking, digital transactions, mobile banking, wallets, and so on. However, booming verticals such as investments, lending, and digital payments are witnessing competition from FinTech startups, digital currencies, and other players.

The major drawback of the current e-banking system is the lack of data privacy. Coupled with operational inefficiency, this leads to customer dissatisfaction. Since banks, at their core, thrive on a massive amount of data and perform repetitive tasks based on it, AI offers the ideal solution for generating sector-wide change. According to a research report by Business Insider Intelligence, the aggregate potential cost savings for banks from AI-based applications is estimated to be $447 billion by 2023.

Here’s how artificial intelligence will change the banking industry:

- Front Office — by enabling conversational banking with the help of chatbots

- Middle Office — by implementing a bulletproof fraud detection and prevention system

- Back Office — by introducing software to efficiently analyze and manage transactions, customers and other data

The wide-scale adoption of AI in banking brings some eye-catching bonuses. AI and machine learning not only enhance efficiency by automating and optimizing error-prone processes, but they also reduce risks and operational costs for banks, detect and prevent frauds, improve customers’ experience through personalization, aid efficient decision-making related to investments or credit-risks, and much more.

Now we will take a closer look at these gains:

Enhanced customer experience

AI in banking encompasses the use of conversational assistants, such as chatbots. These are available 24/7 — unlike employees. Over time, customers have become increasingly comfortable with this automated software for solving standard queries.

With the help of natural language processing technology and machine learning (ML) algorithms, chatbots can also offer personalized suggestions to different types of customers. For example, chatbots can separately notify business customers about loan or merchant banking services.

Reduced risk and operational costs

A Robotic Process Automation (RPA) software performs all the rules-based digital tasks which are otherwise performed by humans. This means RPA takes over all the error-prone and time-intensive tasks, such as entering customer data from forms, contracts, and other sources. This is particularly relevant in the context of emerging technologies like crypto banking solutions, where efficient and accurate data processing is crucial.

When combined with natural language processing, improved handwriting recognition and other AI technologies, RPA bots become intelligent process automation tools that can handle large volumes of tasks previously handled by humans. Consequently, they reduce error rates and operational costs.

Better fraud detection and regulatory compliance

As machines very rarely make errors or fail to detect fraud, AI can help banks track the loopholes in their systems and minimize risk. As transaction volumes and data increase, banks require advanced software and algorithms to crunch more numbers.

AI also enables banks to deploy AI virtual assistants that regularly check the bank data in accordance with regulatory compliance without committing errors. They monitor all transactions, check customer behaviors, and audit and log information into various regulatory systems.

Automating investment decisions and process

Banks also deploy AI-based smart systems to make investment decisions and to underpin their investment banking research. While professionals are kept in the loop, AI systems can study and recommend untapped investment opportunities.

A number of financial service providers are using robo-advisors that understand the needs of clients and offer personalized portfolio-management services at any time of day or night.

Improved loan and credit decision-making

The existing credit system considers factors such as the customer’s credit score, history, and bank transactions. This setup is far from perfect. However, an AI-based loan and credit system can help by studying the behaviour patterns of customers with limited credit history to determine their creditworthiness. Also, the system warns banks about specific behaviors that may increase the chances of default.

Clearly the strategic deployment of AI in banks offers substantial benefits, which frequently outweigh the costs and investments made. But it’s also important to note that AI in banking is a long-term and not a short-term decision.

AI in banking: use cases

Artificial intelligence and machine learning target repetitive manual tasks that are extremely prone to error. It replaces these tasks with software that has the potential to sense, learn, and improve, just like the human mind. Such tasks are present in all areas of banking, including commercial banking, corporate banking, and even investment banking.

Adding AI technology to banking applications enables banks to achieve invaluable customer satisfaction, as AI constantly tracks users’ activities and behaviours to offer them personalized suggestions. The demand for AI functionality in business applications has witnessed robust growth due to its widespread acceptance among users, and these capabilities are often implemented through systems built via banking software development.

AI is a boon for any industry that thrives on data. AI-based bank applications automatically sort, distribute, record, and analyze all collected data. The inferences made are used to offer higher personalization to all users. As a result, AI helps banking institutions to simplify and tackle the challenges related to the collection and analysis of big data.

AI-based banking applications also track users’ search patterns and consequently suggest services and schemes. Thanks to AI, banks generate 66% higher revenue from mobile banking than from their offline customers.

Here are some of the most notable intelligent banking solutions offered by AI:

AI-enabled chatbots

Ever since AI sparked a digital revolution, chatbots have secured their place as the most popular AI use case in almost all industries, including banking.

Chatbots are simply AI-based conversational interfaces: they can potentially automate and replace all straightforward front-office operations, from KYC to customer helplines.

Researchers have reported that financial institutions save up to four minutes for every conversation handled by a chatbot. Chatbots can simultaneously handle thousands of customer conversations on the bank’s app, website, or even social media, thereby relieving front-end workers of a large workload.

Chatbots do not just respond to queries. They also proactively notify customers of new offers, services, payment reminders, credit report updates, portfolio updates, and more. It’s the range and versatility of chatbots that have enabled them to so radically and successfully enhance digital banking.

See how our AI chatbot development services can improve your website efficiency

Immaculate process automation

Banks deal with data and queries from innumerable customers, day in and day out. Manually performing all functions involved in registering customers, addressing their concerns, analyzing information, checking and verifying balances, and myriad other tasks too quickly become mundane and time-consuming jobs, liable to error.

AI automates these repetitive tasks, thereby freeing the employees for more complex jobs. The point of AI is to simplify the functioning of banks and make the whole data and customer-handling process seamless.

Portfolio and wealth management

Advances in AI technology are creating machines as intelligent as the human brain. Machine learning algorithms track all a user’s activities, also studying the various factors that cause movements in the financial markets.

Traditionally, professionals such as portfolio and wealth managers connected with customers to understand their financial goals and draft a personalized financial plan. These days, AI-based banking applications can suggest financial plans for users based on their goals.

The algorithm takes into consideration all market trends, external factors, and sentiments. The upshot is that banks can now rely on AI technology to recommend portfolio and wealth management solutions.

Guaranteed data security

AI-based systems are highly effective in fraud detection and the prevention of data breaches. The software tracks customer behavior, location, and habits, triggering an automatic security mechanism for unusual activities.

According to the Federal Trade Commission, credit card fraud was the most common type of personal data theft in 2020. To prevent theft and data breaches, banks are increasingly adopting AI-based security systems. AI in banking applications promises transactions that are safer and quicker.

Credit risk management

Some of the most challenging tasks for bankers relate to the evaluation of customer creditworthiness. There are certain risks involved in extending credit to borrowers, and every bank appoints a team of professionals to evaluate credit decisions. Despite a thorough assessment of the borrowers’ creditworthiness, banks have to contend with bad debts every year.

In contrast, AI systems are much more precise than humans when it comes to credit evaluation and lending decisions. AI-based systems deploy an algorithm to evaluate customers’ behavior, credit history, and bank transactions to arrive at their conclusions.

Tracking market tendency and trading

AI enables banks to process large chunks of data and predict market trends, stocks and currencies. Advanced machine learning techniques help to evaluate market sentiments and suggest investment options.

AI flags up the best time to invest in stocks and warns when there is a risk. This explains why hedge fund managers use AI-based systems. AI also helps to speed up decision-making, thanks to its very high data-processing capacity. AI makes trading convenient and advantageous for both banks and their clients.

We have looked at just a few of the many applications of artificial intelligence and machine learning in the banking sector. Overall, AI in banking makes banks more reliable, efficient, customer-friendly, and responsive. However, in deciding to adopt AI-based systems, banks need to be mindful of the risks and challenges that accompany them.

Obstacles to the wider adoption of AI in banking

Despite its successful use cases and benefits, certain challenges impede the widespread adoption of AI and machine learning in the banking sector. The biggest issue is a potential lack of a clear AI strategy — in terms of talent, data, and other resources. Other obstacles include the lack of explainability and legal concerns.

Shortage of talent

AI-based banks compete with Fintech and technology companies to recruit experts. They need people who are knowledgeable not only about banking, but also about artificial intelligence. Clearly, it is quite difficult to find such specialists. Banks therefore have to settle for inexperienced individuals and invest time, effort, and cost in training them.

When it comes to the shortage of talent, AI-based banks can consider outsourcing or developing collaborative models with an IT or another technology company to address the talent gap.

Shortage of quality data

Banks need structured production data in the process of training and validation before deploying a full-scale AI-based banking app. Good quality data is required to ensure that the algorithm applies to real-life situations. What’s more, if data is not in a machine-readable format, it may lead to unexpected AI model behavior.

Thus the quality of this data determines the quality of the AI model. Additionally, banks have to be mindful of risking customers’ private data for testing and validation. As a result, banks accelerating towards the adoption of AI need to modify their data policies to mitigate all privacy and compliance risks.

Lack of explainability

AI-based systems are widely applicable in decision-making processes as they eliminate errors and save time. However, they present a ‘black-box’ threat, meaning they may follow biases learnt from previous cases of poor human judgement. Minor inconsistencies in AI systems do not take much time to escalate and create large-scale problems, risking the bank’s reputation and functioning.

To avoid calamities, banks should offer an appropriate level of explainability for all decisions and recommendations presented by AI models. Banks need to understand, validate, and explain how the model makes decisions.

Legal concerns

A number of customer-privacy regulations such as the Personal Data (Privacy) Ordinance (PDPO), the EU’s General Data Protection Regulation (GDPR), or the California Consumer Privacy Act affect banks developing an AI model. Banks are required to be transparent while profiling customer data and make it machine-readable for automated decision-making.

Banks, therefore, should always get customers’ consent before sharing any personal data. They should gauge all activities for potential legal risks and set up adequate guidelines to mitigate such risks.

Lastly, industry regulators must set up guidelines and certification processes for recognizing and assessing companies that adopt these new technologies. Such steps will ensure standardization and provide a framework for the governance of AI technology in banks, thereby encouraging broad adoption of this technology in the banking sector.

Take a look at this AI-based shared grocery shopping list application

How to become an AI-first bank

Every new technology presents novel challenges before it becomes widely adopted. On the other hand, there are risks too in avoiding the adoption of any disruptive technology (like AI).

According to Business Insider Intelligence, ‘Millenials and Gen-Zs are becoming banks’ largest addressable consumer group in the US,’ with close to 78% of millennials never going to a brick-and-mortar bank. The same source also estimated that 4 out of 5 bank account holders will use digital banking solutions by 2024. Therefore, banks must adopt a holistic approach by implementing this futuristic technology and so avoid the risk of becoming irrelevant.

While many still believe that AI is an experimental technology for banks, there exists a range of successful real-world examples of AI implementation in this industry. Some pilot programs never moved on to large-scale deployment. But even so, banks should capitalize on AI before it’s too late.

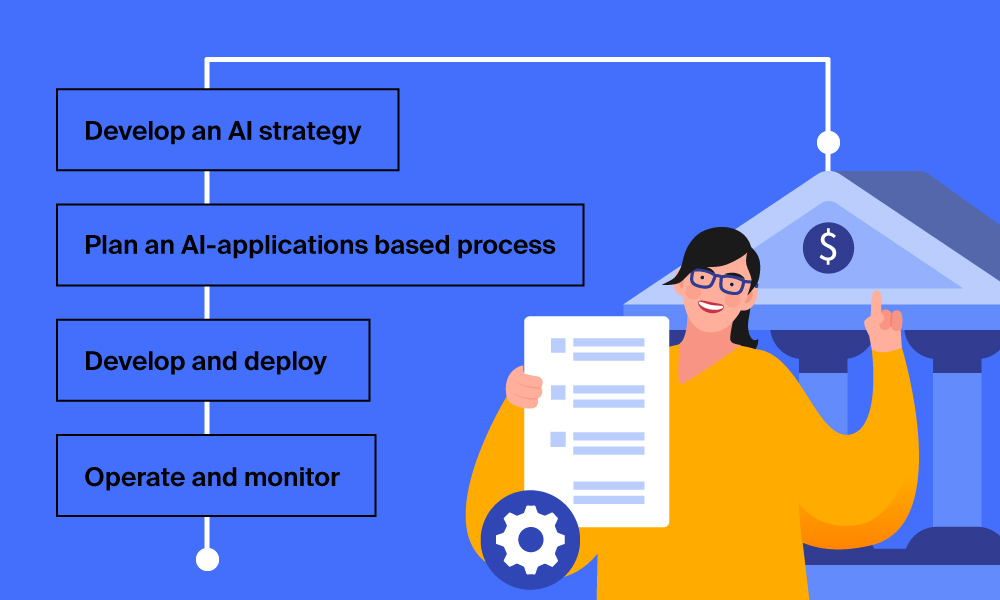

Now we will look at some steps that banks can take to evolve their processes and adopt AI on a broad scale while paying due attention to the four critical factors — people, governance, process, and technology.

Develop an AI strategy

The AI implementation process begins with developing a corporate-level AI strategy:

- Conduct internal market research to find gaps among the people and processes that AI technology can fill. Formulate a corporate-level AI implementation strategy, keeping in mind the values and goals of the organization.

- Ensure that the AI strategy complies with the regulations and industry standards. Banks can also evaluate the existing international industry standards.

- The final step in strategy formulation is to refine the internal policies and practices related to data, talent, infrastructure, and algorithms to provide clear directions and guidance for adopting AI across the bank’s various functional units.

Plan an AI-applications based process

The next phase involves identifying the highest-value AI opportunities, aligning with the bank’s processes and strategies. Banks must also determine the extent to which they need to deploy AI solutions within existing or modified operational processes.

After identifying the potential use cases, the business and technology teams should run feasibility checks. They must examine all aspects and identify the gaps for implementation. Based on their evaluation they must select the most feasible cases.

The final step in the planning stage is to map out the AI talent and determine an implementation model. Banks require a number of experts, such as data scientists or algorithm programmers for the development and implementation of AI solutions. If they lack in-house experts, they can outsource or collaborate with a technology provider.

Develop and deploy

After planning, banks come to the execution stage. Before developing fully-fledged systems, they need to create prototypes to understand the shortcomings of the technology. To test these prototypes, banks need to source relevant data and feed it to the algorithm. The AI model builds and trains on this data, so it’s important that the data is accurate.

As soon as the AI model is trained and ready, banks must test and evaluate it and interpret the results. A trial like this helps the development team to gauge how the model will perform in the real world.

The final step is to scale up the trained model in order to deploy it enterprise-wide. Once deployed, production data starts pouring in. With more production data, routine checks, and customer feedback, banks can regularly improve and update the model.

Operate and monitor

Unlike traditional IT applications, AI solutions require continuous monitoring and calibration. Banks need to design a review cycle to monitor and evaluate the functioning of the AI model comprehensively. These actions will help banks in the robust execution of operations and management of cybersecurity threats.

At the operation stage, the continuous accumulation of new data will affect the AI model. Therefore, banks should take appropriate measures to ensure the quality and fairness of the input data.

Find out more about this AI-based solution for human retina image recognition

Principles for ethical governance of AI

The above steps towards the wide-scale adoption of the AI model in banks cover all the core factors (people, process, and technology) except governance. Since chatbots or ML-driven prediction systems make decisions, banks need to establish ethical governance or risk management frameworks. The principles that form the foundation of this ethical governance framework are as follows:

Fairness

Banks should continuously check the production data for any biases. A minute bias in the AI model can progress to a major incident in very little time. This is why banks should be especially careful in the training stage of the AI model.

Robustness and security

AI models are adaptive, not rigid. ML algorithms are constantly studying behavior, learning from external factors and modifying themselves to deliver improved results. Therefore, AI models require constant monitoring and validation of decisions by the bank.

Banks should implement cybersecurity measures to avoid or control potential cybersecurity threats, such as data poisoning and adversarial attacks. Some tools that banks can use to test the robustness and security of the AI system include the Model Stability Assessment Tool, API Theft Assessment Tool, and Synthetic Data Generator.

Control and compliance

The banking sector is highly regulated. Therefore, banks should constantly check their regulatory environment and understand how AI can shape their future business practices. They should check compliance with local and national regulatory authorities as well as international agencies.

Explainability and interpretability

Governance rules require banks to be in a position to explain to their stakeholders all decisions made by the AI model. Banks need to implement adequate measures during the design phase itself to ensure the desired level of explainability.

What’s more, the decisions made by the AI model should be interpretable to the developers as well as the bankers. Lack of explainability and interpretability are barriers to the widespread adoption of AI in banking, as they cause a ‘black-box’ threat.

These principles lay the foundation of ethical governance during the implementation of AI-based systems in banks.

Get more details about this smart retail solution powered by AI & iBeacon technology

Real-world examples of AI in banking

Many personal, consumer, and corporate finance organizations have adopted AI in their operations and improved their efficiency. However, many banks still treat AI as a stand-alone initiative and not as a foundational concept. At the same time, there are world banks that are setting the ball rolling for this technology in the financial sphere.

JPMorgan Chase

JPMorgan is leading the way in holistic AI adoption. The bank has undertaken rigorous investments and aggressive hiring, alongside a comprehensive approach to implementing AI across all operations. Chase has carried out extensive research in the field of AI in banking. It will use its research findings in six applied initiatives, namely:

- Anomaly detection

- Smart documents

- Intelligent pricing

- Virtual assistants

- News analytics

- Quantitative Client Intelligence

For Chase, Q consumer banking accounts for over 50% of its net income. With this in mind, the bank adopted AI-based fraud detection algorithms for its account holders. It was the bank’s contribution to AI and increased value to customers that earned it second place in Insider Intelligence’s 2020 US Banking Digital Trust survey.

Bank of America

Bank of America has been investing seriously in AI and machine learning since 2017. At first, they introduced a virtual banking assistant, Erica, to their banking application. Erica helps customers to manage their bank accounts and keep track of their spending habits.

In the second half of 2020, Bank of America began using AI in credit risk analysis. They deployed the natural language processing technology that estimates a client company’s probability of defaulting within 12 months.

Bank of America is reportedly also researching new ways they can leverage AI in banking operations, from fraud detection and anomaly detection to investment-related decision-making.

Capital One

Capital One’s intelligent virtual assistant, Eno, is the best example of AI in personal finance. Besides Eno, Capital One is creating benchmarks for the use of AI in their industry. They use virtual card numbers to prevent credit card fraud. Meanwhile, they are working on computational creativity, which involves training computers to be creative and explainable.

Capital One was also among the first banks to adopt a virtual assistant in their banking application, back in 2017. Since then it has been a leader and innovator for deploying scalable AI innovations into banking operations.

Besides commercial banks, a number of investment banks like Merrill Lynch and Goldman Sachs have also welcomed and integrated analytical AI-based tools in their routine operations. Many banks, investment firms and Fortune 500 (financial) companies use an AI-based search engine called Alphasense that deploys natural language processing to analyze keyword searches and discover market trends.

Conclusion

Artificial Intelligence and Machine Learning technologies have already provided a great array of intelligent solutions across all major industries, including finance. The COVID-19 pandemic ramped up the adoption pace of these technologies even further. Experts believe that AI can have a profound impact even in the banking sector, saving up to $1 trillion by 2030.

AI is all set to bring about a radical transformation. Banking professionals believe it is an opportune moment to ride the AI wave: economic fundamentals are strong, the regulatory climate is favorable, and transformation technologies are more readily accessible and powerful than ever.

Is your bank prepared to face the fresh challenges of tomorrow? If you believe that now is the right time to roll out AI solutions for your banking operations, contact our team of professional ML consultants and AI developers. We can handle your AI-based process automation and help your bank stay ahead of the competition.