Financial platforms, sports and health apps, transportation solutions, and even voting systems — blockchain now serves as a solid basis for them all. But is blockchain always the ideal solution, or are there exceptions? Let’s examine the tech inside out.

Blockchain has proven to be a reliable technology for many areas beyond financial transactions. It can accelerate business growth by eliminating third-party services, helping track important data in a matter of seconds, and reducing security risks. It is indeed a transformative technology if used wisely.

On the other hand, the technology is so popular that many companies simply follow the trend and launch blockchain projects without conducting blockchain feasibility analysis and assessing whether the blockchain will really benefit their future solution.

To make the right decision, your company should know how blockchain technology works, what its benefits and drawbacks are, and in what cases blockchain does make sense.

Read this article to learn about all these aspects in detail and understand if blockchain is the right technology for your project.

Blockchain and its types in a nutshell

Blockchain has been around since 2008 and has evolved a lot over the years thanks to the contributions of many developers and tech enthusiasts.

The name of this technology speaks for itself — blockchain is literally a chain of blocks, where each block is tied to the previous one by means of a cryptographic hash. The blocks storing transaction information are decentralized: there is no central authority controlling the system.

There are basically two types of blockchain: permissioned and permissionless.

A permissioned blockchain cannot be accessed without permission. These blockchains are not public and have limited decentralization. Users are only allowed to perform specific actions granted by the system administrators.

Permissioned blockchains are therefore well suited to enterprises that need to keep their information private and require a certain level of centralization.

A permissionless blockchain, on the other hand, is publicly accessible and fully decentralized. Any user can join and interact with the network without requiring special permissions. If you want to launch an application for digital asset trading, crowdfunding, or decentralized storage, a permissionless blockchain would be a great fit.

Bitcoin, Solana, Cardano, and Ethereum are the most popular permissionless blockchains. At the same time, Ethereum can also be used to develop private blockchain-based platforms. Polkadot is another example of a blockchain that can be applied to transfer data across both public and private blockchains.

What are the benefits of blockchain?

Blockchain technology is famous for its decentralized storage, transparent data, immutability, and increased security. Let’s take a closer look at each of these features.

Decentralization

Blockchain is decentralized by default. This feature, usually seen as a benefit, means that there is no single person or organization managing the entire system.

With centralized networks, all information is generally stored on one server and controlled by a single team. Consequently, such systems are much easier to tamper with as they contain a single point of failure.

When a platform is decentralized, all data is distributed among multiple network nodes in different locations. Each node has a copy of the same data in the form of a distributed ledger. If someone even tries to alter one block, it will simply be rejected by the other network participants.

Transparency

Blockchain technology provides transparency of data. Every single action in the network is visible and can be tracked.

For example, if you use blockchain in your supply chain, it will be easy to follow every step of the transportation process, and you can track each item to where it comes from in a few seconds. As for financial transactions, users can track where each coin goes.

Immutability

Blockchain’s immutability means that once a new block of data is added and stored on the blockchain, it cannot be modified or deleted. This is a prominent feature because it prevents any participant in the system from changing the data for their own purposes.

Security

While technology that’s 100% secure has not been invented yet, blockchain can still boast of its powerful security features. Blockchain-based platforms are secured through decentralization and strong cryptography.

Nevertheless, users also need to take simple protective measures. For example, they should avoid sharing their private key, create a unique password and never store it online, and enable two-factor authentication.

Other benefits of blockchain technology include faster settlements, trust, and reduced costs by eliminating multiple intermediaries.

In what industries does blockchain make sense?

The global blockchain market is growing by leaps and bounds. According to the Blockchain Market Analysis Research Report, it is estimated to reach $104.19 billion by 2028, with a CAGR of 55.8% from 2021 to 2028.

The report also states that blockchain technology is most widely used in industries such as banking, financial services, insurance, transportation, healthcare, government, telecommunications, energy and utilities, and retail and consumer goods.

The industries where blockchain’s trust, transparency and the ability to track data correctly are especially essential are transportation and supply chain, healthcare, and government.

Blockchain-based supply chain solutions help track where goods come from and record all data in chronological order. All participants in the supply chain can check that everything is going well and how a particular item is being transported from the manufacturer to the store shelf.

For example, IBM’s blockchain-based solution Food Trust showed impressive results when it was used to track mangoes and pork from their origin to a Walmart supermarket. The time it took to trace the provenance of these items reduced from 7 days to 2.2 seconds.

Why is blockchain important here? Because fast tracking helps organize product recalls and prevent customers from getting foodborne diseases.

How Walmart Strives for Food Quality And Safety Using Blockchain Technology Solutions

Find out how PixelPlex consultants helped their client analyze the feasibility of implementing blockchain in a shipper-to-carrier direct freight network

Pharmaceutical companies can also apply blockchain solutions to track medicines. This will ensure that the items are delivered in the proper condition and are not counterfeit.

Blockchain can also be used to create, store, and update electronic health records (EHR) and give patients more control over their own health data.

MediBloc, a blockchain-powered healthcare information ecosystem, does just that. The project includes the MediPass mobile app that allows patients to collect their medical records scattered across different hospitals in one place, and provide them with data sovereignty. The project has 20 partnerships with medical institutions, won two prestigious healthcare awards, and attracted $3.5 billion in Series A investment.

As for blockchain applicability for government, blockchain voting projects are becoming more and more popular.

The Korean Ministry of Science and Technology, along with Korea’s Internet and Security Agency, are about to introduce blockchain for online voting. The Korean government has recently approved a pilot blockchain-powered voting system that can potentially be used by more than 10 million people.

If we look at the possibilities of working with digital assets, the real estate industry would be a perfect example. Blockchain in real estate allows you to tokenize real-life property and buy or sell it in fractions in the form of tokens.

Blocksquare, Liquefy, Securitize, and Harbor are just a few of the many real estate tokenization platforms that help property owners tokenize and sell their assets.

What are the disadvantages of blockchain?

As Stephen Hawking said, “One of the basic rules of the universe is that nothing is perfect.” Unfortunately, blockchain is not perfect either and it does have several drawbacks. Here are the main ones:

- Scaling issues

Blockchain-based solutions may not be as fast as traditional systems because many computers with servers in different locations are involved in the transaction validation process.

The blockchain that is infamous for its scalability problems is Ethereum. On average, it processes only 13.7 transactions per second (TPS). In addition to this, if the network is flooded with users, transaction speed slows down and transaction costs increase significantly. However, there is still a chance that the situation will improve when the blockchain upgrades to Ethereum 2.0.

Meanwhile, more and more new blockchains are emerging. In 2021, Solana grabbed the tech community’s attention as a blockchain capable of processing up to 65,000 TPS. This is very close to the number of transactions Visa can handle.

So we can see that the technology is evolving and will probably soon be able to catch up with traditional systems.

Check out a comprehensive comparison between Ethereum and Solana

- Immutability challenges

You might be wondering why immutability is listed as an advantage and disadvantage at the same time. Well, it depends on your needs and requirements.

If you want to have a transparent system where all changes are recorded as new blocks and can be tracked, then immutability is definitely a big plus. However, if reversibility is a desirable feature, blockchain cannot provide it.

- Difficulty of development

Blockchain is quite complex. To create a robust blockchain solution, developers need to know a certain programming language, for example Solidity for Ethereum, and write smart contracts extremely carefully.

The problem is that once smart contracts are deployed, they can’t be fixed and mistakes will then cost money. It is also necessary to understand cryptography to ensure a high security level for the application.

Therefore, to avoid mistakes and create a robust application, any blockchain-based solution must be developed by proven professionals with an impressive portfolio of successful launches.

When should you use blockchain and when is it better not to?

Blockchain is a very specific technology that solves very specific problems. It is not yet a universal technology that would allow you to achieve any business goal, so it is important to know in which cases you can really consider implementing blockchain, and in which it is better to give up on the idea.

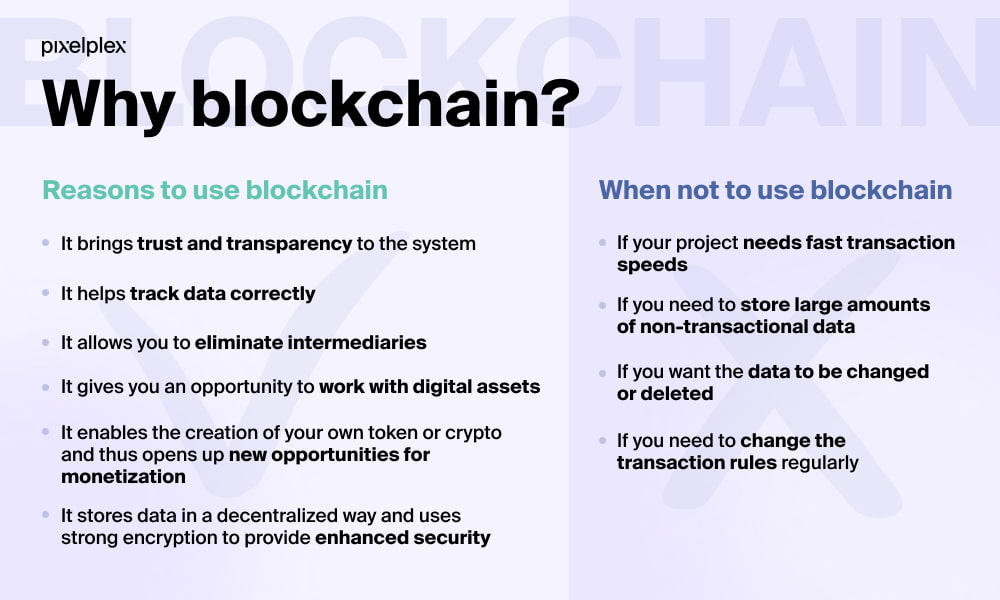

Reasons to opt for blockchain

First things first. Let’s analyze the situations where blockchain would be the ideal solution.

You need to bring trust and transparency to the system

Blockchain came into our lives and became popular after the introduction of Bitcoin. At the very beginning, blockchain served only as a platform for hosting and exchanging this digital currency, but in such a way that its movement could be tracked and users could interact with each other directly without any intermediaries.

All in all, blockchain was designed to provide transactional transparency and solve the problem of mistrust between parties. So, if you want your future platform to be transparent and thus provide trust between users, then blockchain is the best choice.

You need to track data correctly

Smart contract functionality is the core of blockchain technology. Simply put, a smart contract is a piece of code that defines the terms of each transaction. The transaction is carried out only when certain conditions are met. After that the transaction data cannot be changed.

Let’s say you are a sports event organizer and you want to use blockchain for selling basketball tickets. Smart contracts can be written in such a way that your company and the basketball teams receive a percentage of ticket resales.

You need to eliminate multiple intermediaries

If your business involves many intermediaries that only bring inefficiencies to your work processes and waste your time and financial resources, blockchain technology can help you tackle this issue.

For example, if we take a look at the real estate industry, a lot of third parties are involved. They can make the process of buying and selling real estate complex, cumbersome, and expensive.

If real estate data is stored on the blockchain and the terms of transactions are written in smart contracts, buyers and sellers can easily access this information, verify ownership, view transaction history, and purchase or sell property without turning to real estate agents.

All in all, the process becomes less time consuming and less expensive as buyers and sellers negotiate directly.

You want to work with digital assets

Blockchain and digital assets are made for each other. Blockchain allows you not only to host, buy, and sell digital assets, but also to tokenize real-world items such as real estate and gold, and sell them as tokens.

Thanks to blockchain technology and tokenization, it is possible to divide assets into many parts and thereby ensure greater accessibility and liquidity of various types of assets. Not everyone can afford to invest in an entire commercial building, but if the property is split into multiple tokens, more people will be able to invest in it.

Did you know that you can even tokenize yourself? Find out exactly how it can be done

You want to enhance security by storing data in a decentralized way

Centralized systems and databases provide a single point of entry for potential cybercriminals. When the system is decentralized, the nodes, computers, and servers are located in different places and they are much more difficult to hack.

If you still want to keep control over your enterprise network, you can choose to use a permissioned type of blockchain that implies limited decentralization.

Why blockchain is not always the best solution

Blockchain is a unique technology, but not perfect. If you’re still in two minds, these points will also help you understand if blockchain is the right tech for you:

- Blockchain is not as fast as traditional centralized solutions

If your business requirements include extremely fast transaction speeds and you are not ready to invest in massive computing power to run your blockchain-based platform, then blockchain might not be the best choice.

- Blockchain is not designed to store large amounts of non-transactional data

Blockchain basically involves the recording and storage of transaction data, plus information about the creation and transfer of tokens and digital IDs, as well as certificates such as diplomas and other papers.

- Once the data is recorded, it is impossible to change it

If you want to be able to fix or delete data, then it’s better to consider other technologies, as blockchain cannot provide this functionality.

Questions to ask before making a decision

And finally, ask yourself these eight questions before making a decision on blockchain implementation:

- Do you need your system to be transparent?

- Is your business looking to eliminate middlemen from your workflows?

- Does your system have a database?

- Do you want to launch your own token or cryptocurrency to open up new monetization opportunities?

- Do you want to work with digital assets?

- Do you want to create a smart transaction system with immutable smart contracts?

- Do you need to record each step of the transaction process and store this data forever?

- Is there lack of trust between the parties that you plan to bring to your platform?

If you answered “yes” more than four times, you can consider making this technology the basis for your future project.

Blockchain Database vs Traditional Database: Choosing the Best For Your Project

Final thoughts

To use blockchain or not to use — that is the question. Although blockchain is not a panacea for every tech-related problem, it does have numerous benefits that make it a suitable technology for a range of industries. Even if you didn’t find your company’s industry listed above, you can become a pioneer in your field and be the first to innovate.

The implementation of blockchain technology is a complex process and requires professional help. If you want to learn more about blockchain technology, or are even ready to start developing your own blockchain product, get in touch with the PixelPlex blockchain team.

Our blockchain development company has delivered more than 60 blockchain-powered applications and would like to help you, too, enter the world of decentralized technology. Share your idea and we will come up with an effective solution tailored to your business needs.