The popular appeal of cryptocurrencies and stablecoins is steadily increasing. As take-up rises, central banks across the globe have realized that they need to provide their own alternative — a central bank digital currency, also known as CBDC.

According to the Atlantic Council data, all the G7 economies are preparing to launch their own central bank digital currencies.

The International Monetary Fund has estimated that there were about 100 CBDCs in research or development stages as of July 2022. Two are already officially launched: the eNaira in Nigeria and the Bahamian Sand Dollar.

To help you better understand what CBDC is, our team has prepared a detailed guide to cover all your FAQs. Check it out.

What is a CBDC?

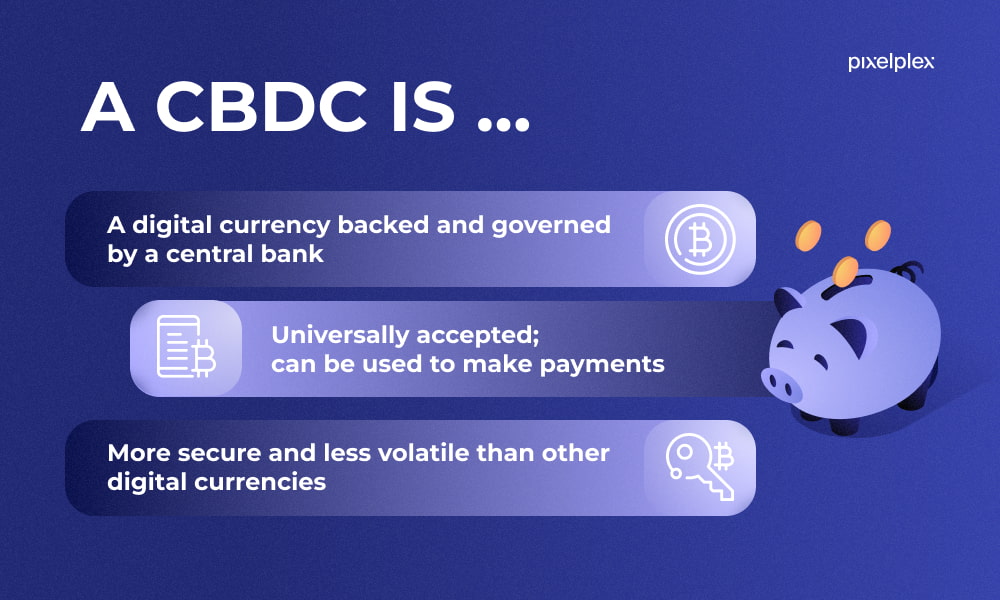

A CBDC is a digital currency that is backed and issued by a central bank. Digital currencies are pegged to the value of the country’s fiat currency and are used by households and businesses to make payments.

A CBDC currency is:

- Digital

- Universally accepted

- Issued by a bank

It’s worth mentioning that a CBDC is not a cryptocurrency, like Bitcoin, for example, which is governed by distributed autonomous organizations. Nor is it equivalent to electronic cash.

Rather, a CBDC is traditional money but in a digital form. It is influenced in terms of supply and value according to the country’s monetary policy and the central bank. It is this that makes CBDCs more secure and less volatile compared to other digital currencies on the market.

At present, there are two main types of CBDCs: general-purpose CBDCs and wholesale-only CBDCs.

- General purpose CBDCs are the ones that are distributed to the general public. Based on the distributed ledger, they will offer anonymity, traceability, 24/7 availability 365 days a year, and the capacity for an interest rate application.

- Wholesale CBDCs are for banks that keep reserve deposits with a central bank. These CBDCs can potentially increase the efficiency of payments and securities settlements while reducing liquidity risks. With a restricted-access digital token, wholesale CBDCs will be able to supplement or replace central bank reserves.

How does a CBDC work?

Being a digital representation of a country’s fiat money, CBDCs work just the same way. As soon as the central bank issues its CBDC, it can be used as legal tender for transactions, such as making purchases, paying salaries, and so on.

In contrast to traditional processes, the CBDC transaction won’t need to pass through numerous banks, which can take several business days.

The transaction will occur instantly on the digital ledger. Moreover, the transaction cannot be reversed, so if someone sends you $100, for example, you will have it in your account almost instantly and it cannot be taken back.

Find out how blockchain adds value to the financial organizations

What are the benefits of CBDCs?

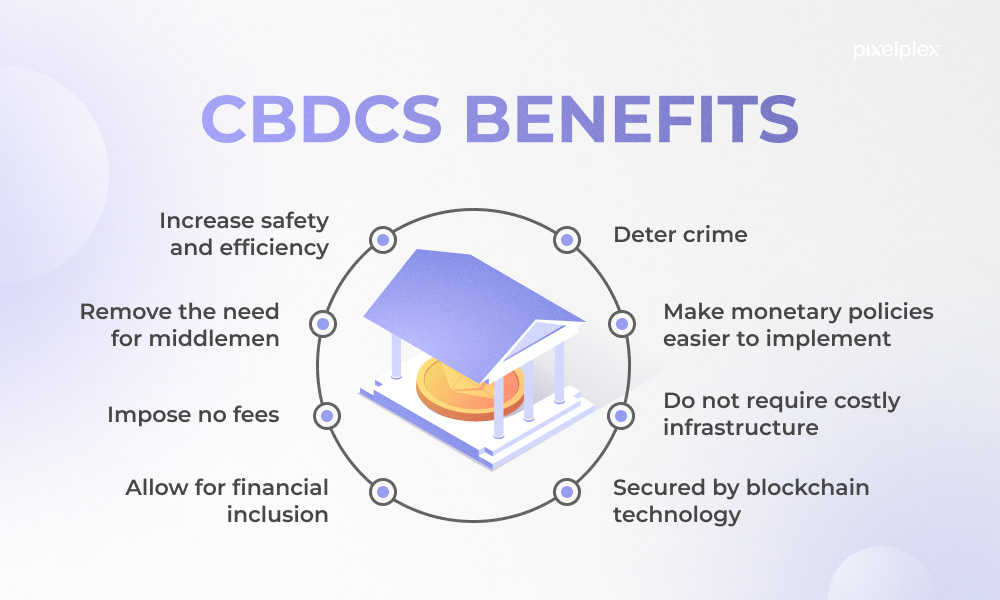

A CBDC can help increase the safety and efficiency of both wholesale and retail payment systems while removing the need for middlemen and instead connecting with individuals directly. However, there are much more benefits than that, including:

CBDCs deter crime

CBDCs deter crime and eliminate the danger of fraudulent third-party activities, as the central bank handles any remaining risk in the system. Moreover, as all transactions are stored digitally, the central bank can easily trace them back to their source, meaning that it is difficult to use the tokens for malicious activities.

CBDCs make monetary policies easier to implement

Central bank digital currencies make it easier to implement government and policy functions. They can help reduce the work required to fulfill such functions as monetary policy, distribution of benefits, tax collection, and direct deposits to individuals.

There are no fees with CBDCs

There are no fees charged for CBDC transactions, including payments and transfers. The implementation of a CBDC can help reduce costs for banks and merchants, because fees associated with cash handling and securing will no longer be an issue.

CBDCs allow for financial inclusion

You don’t need to open a bank account to have a CBDC wallet. As a result, people who are underbanked or unbanked can still become part of the financial system. They will be able to create a transaction history and use it to gain access to loan financing by spending, transferring and receiving a CBDC.

There is no need for costly infrastructure

Since central bank digital currencies can create a direct link between customers and central banks, there is no longer a need for expensive infrastructure, which leads to reduced costs.

CBDCs are secured by the blockchain technology

CBDCs rely on blockchain technology, which is generally considered to be more secure for financial transactions than traditional centralized technologies.

How will a CBDC affect banks?

Assuming CBDC initiatives progress beyond the pilot stage, central banks are likely to continue building all the necessary tools and infrastructure necessary for the CBDC’s further development.

The successful implementation of a CBDC can potentially displace a material share of deposits held in commercial bank accounts. It can also create competition for current payment solution providers.

At the same time, commercial banks are likely to play a crucial role in the large-scale adoption of CBDCs due to their knowledge of customer needs and behavior. Commercial banks are well-versed in client onboarding and the execution of transactions, and therefore it is likely that the success of the CBDC model will largely depend on both commercial and central banks collaborating.

This is why commercial bank leaders would be advised to collaborate with central banks to learn more about CBDC initiatives and shape future models together.

Want to enable digital transformation in your banking or financial organization? Here’s how to do it right

How to invest in CBDCs?

Since CBDCs will be issued in the same way as the nation’s existing monetary supply, there is no profitable route for CBDC investments. Put simply, investing in a CBDC is just like getting a country’s banknotes.

It’s also worth pointing out that at present foreign nationals cannot hold central bank digital currencies of any other country in their digital wallets. For example, if you are a US citizen, you cannot access the Bahaman Sand Dollar.

What is CBDC in crypto?

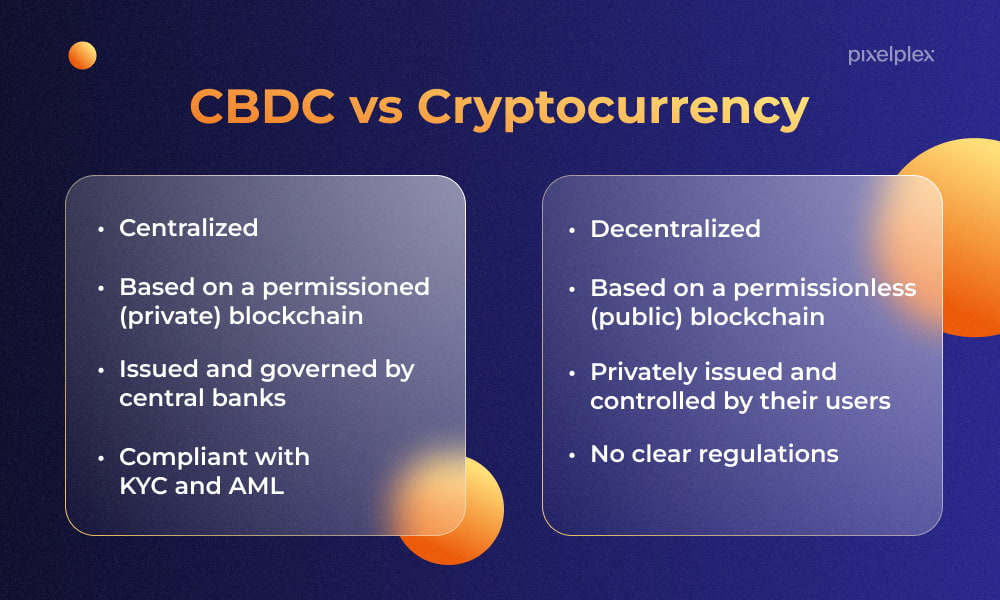

CBDC is commonly confused with cryptocurrency, yet they are not interchangeable terms and a central bank digital currency is not a cryptocurrency. Here’s why:

- CBDCs are centralized and governed by central banks while other digital currencies are decentralized and controlled by their users.

- In contrast to CBDCs, cryptocurrencies cannot be regulated by single authorities.

- CBDC is a digital version of the country’s national currency whereas cryptocurrency is privately issued.

- CBDCs rely on permissioned (aka private) blockchains while cryptocurrencies employ permissionless (aka public) blockchain technology. The main difference here is that all transactions on the public blockchain can be read and audited by any party whereas the private blockchain functions as a closed and secure database based on cryptography principles.

- CBDCs would be less concerned about data and privacy and any stockpiling would be prohibited. Cryptocurrencies can be used for both financial operations and speculation purposes.

How is CBDC different from fiat?

Both CBDC and fiat currency are government-backed forms of money. The only difference is that fiat money is printed and held physically in the form of coins or bills while CBDC is presented as an electronic record or digital token.

However, CBDCs offer several advantages compared to fiat money:

- CBDCs can be sent directly to other individuals or organizations without having to rely on third-party payment processors.

- CBDCs can replace cross-border payment systems, being a faster and cheaper alternative.

- CBDCs can ensure a more efficient implementation of a monetary policy by enabling the government to have more control over its circulation.

What blockchain will CBDC use?

Tao Zhang, a corresponding author at the School of Cyber Science and Technology at Beijing’s Beihang University, points out that Ethereum, Corda, Quorum, and Hyperledger Fabric are expected to be the most widely used blockchains for CBDC issuance. Their key applications include inner-bank payments, inter-bank payments, and cross-border payments.

Due to its developed infrastructure, the Ethereum blockchain is currently one of the most suitable blockchains for supporting CBDC initiatives. For example, Norway’s central bank, The Norges Bank, announced that their CBDC prototype infrastructure would be based on Ethereum.

Another technology that already offers a complete solution for minting, managing, transacting, and destroying central bank digital currencies is Ripple. In November 2021, it partnered with the Republic of Palau to develop its government-backed USD CBDC. Then, in October 2022, it started exploring the possibility of developing a digital USD that can be used for instant cross-border payments.

What countries have CBDC?

As of March 2022, there are only a few countries that had actually launched publicly-available CBDCs, mostly existing in the form of proof-of-concept projects. These countries include:

- China. China’s digital yuan gained traction in 2020 when they announced the testing of their CBDC prototype in the Luohu district of Shenzhen. In 2021, they launched the second pilot program in Suzhou City. In January 2023, China’s digital yuan was first used to buy securities.

- Sweden. Swedish Riksbank, one of the world’s oldest banks, launched e-krona to test CBDC. The pilot phase was launched in 2021, followed by the second pilot phase in 2022. The bank announced that it would continue testing e-krona in 2023 and investigating its effects on the Swedish economy.

- The Bahamas. In 2020, the Bahamas deployed their CBDC project called Sand Dollar in two districts: the Exuma and Abaco Islands. Each Sand Dollar constitutes an additional digital variant of the Bahamian dollar.

- The Eastern Caribbean Area. The Eastern Caribbean Central Bank launched the DXCD project to reach financially excluded parts of the population. The prototype is now being tested in Antigua, Barbuda, Grenada, Saint Lucia, St. Kitts and Nevis.

- The Marshall Islands. In 2018, the Republic of the Marshall Islands passed a law which made Sovereign (SOV) the new legal tender.

When will CBDC be released?

Currently, each country has its own path to CBDC. In 2023, more than 20 countries will take significant steps towards testing CBDC, according to the Atlantic Council. Australia, Brazil, India, Russia, South Korea and Thailand are among the countries that plan to continue or pilot testing in 2023.

The United States is currently researching CBDCs to enhance its domestic payments system while reducing costs. In March 2022, President Biden directed federal agencies to evaluate the infrastructure necessary for issuing a US CBDC.

The Bank of England continues to research the implementation of CBDC. In 2021, it set up a Central Bank Digital Currency Taskforce to coordinate the exploration of a potential UK CBDC.

The Bank of Canada is likewise investigating the potential of implementing a Canadian CBDC. The Bank of Canada governor stated that a public consultation into a potential Canadian CBDC will take place in 2023.

The Central Bank of Brazil plans to introduce CBDC by 2024, as confirmed by President Roberto Campos Neto at a conference hosted by Brazilian news site Poser360.

In September 2022, the Reserve Bank of Australia released a white paper in which it announced that the bank would test CBDC use cases and conduct a pilot project for eAUD between January and April 2023.

How to launch a CBDC?

A CBDC launch can broadly be divided into four key steps, including research and exploration, design and testing, implementation, and scaling up. Overall, CBDC deployment can take from 3 to 5 years depending on the chosen development methodology (for example, Waterfall or Agile). We will take a closer look at each step.

Research and exploration

This involves evaluating the potential and feasibility of a central bank digital currency. Here you need to analyze the potential benefits and use cases of CBDC, explore existing projects, and assess possible risks. You will also need to analyze and select a blockchain platform suitable for CBDC implementation.

Design and testing

During the design stage, central banks need to define CBDC functions and features as well as determine the underlying technologies. They will also have to draft CBDC rules.

Each digital currency must have a similar structure that will include an issuer, a service provider, a ledger, and users. As for the key elements of CBDC, these should include:

- Core rulebook encompassing the key principles of CBDC transactions and outlining governance, risk management, access and other participant requirements.

- The infrastructure needed for issuing, redeeming and settling CBDC on the CBDC ledger.

- Processing services, such as payment pre-check, authorization, verification, validation, screening (e.g. security checks), and data and analytics.

- Payment services that involve interaction with end users and include pre-transaction (user onboarding), transaction (payment authentication, customer service and support), and post-transaction (payment advice statements).

- Use case arrangements comprising business and technical rules that determine how each specific use case will work.

Implementation

When launching CBDC to the public, it is generally recommended to start with the development of an MVP to test the selected areas and use cases on the market and then add new functionality based on the results of this step.

Scaling-up

This involves monitoring market adoption of CBDC, getting feedback, and clarifying needs and preferences. Based on this information, banks can enhance your solution with required features and use cases.

Find out how PixelPlex built a community-governed DeFi platform focused on lending, staking, governance, and launchpad services.

Closing thoughts

Although the concept is still in its infancy, a well-designed CBDC has all chances to disrupt the current financial and banking systems by reducing costs, adding further security, enabling financial inclusion, and making monetary policies easier to implement.

Many countries, including the USA, UK, China, Canada, Australia, Sweden and Brazil have already piloted or are currently exploring CBDC projects.

If you are researching CBDC implementation options or evaluating blockchain capabilities for your banking or financial organization, just send us a message. With 450+ projects in our portfolio, our talented blockchain consultants will guide you along the best route to successful project implementation.

Disclaimer: The information provided in the article is for educational purposes only. It does not constitute advice or recommendations for developing or investing in CBDC. Please seek professional advice before taking financial risks.